.png)

Cash flow challenges can strike any business at unexpected moments. A business line of credit for cash flexibility offers a financial safety net that lets you access funds when needed while paying interest only on what you use. This revolving credit solution provides the liquidity many businesses need to navigate short-term gaps and maintain steady operations.

Essential Tips for Maximizing Your Credit Line

Getting the most from your business line of credit for cash flexibility requires strategic thinking about timing and usage. Here are key approaches that can help optimize this financing tool for your business needs.

- Borrow only what you need: Since you pay interest solely on funds you draw, resist the temptation to access the full credit limit unless necessary. This approach keeps costs manageable while preserving available credit for genuine emergencies.

- Plan for seasonal fluctuations: Many businesses experience predictable cash flow dips during certain months. Use your line of credit to bridge these gaps rather than scrambling for emergency funding when revenue drops.

- Monitor your credit utilization: Keeping your balance below 30% of your total limit may help maintain better business credit scores. This practice also ensures you have substantial funds available for unexpected opportunities or challenges.

- Pay down balances quickly: The faster you repay drawn amounts, the less interest you accumulate. Consider making payments as soon as cash flow improves to minimize overall costs.

Smart Strategies for Short-Term Cash Management

Effective short-term cash management strategies often combine multiple financing tools to create a comprehensive approach. A business line of credit serves as one component in this broader financial strategy.

- Create a cash flow forecast: Tracking your expected income and expenses helps identify when you might need to tap your credit line. This proactive approach prevents last-minute financial stress and allows for better planning.

- Maintain multiple funding sources: Relying solely on one financing option can limit your flexibility. Consider how revolving credit benefits complement other funding methods like merchant cash advances for different business scenarios.

- Build relationships with lenders: Establishing strong connections with financial institutions can lead to better terms and faster access to credit when you need it most. Regular communication helps lenders understand your business better.

- Review terms regularly: Credit line terms and your business needs may change over time. Periodically assess whether your current arrangement still serves your cash flexibility requirements effectively.

Steps to Qualify for Business Credit Lines

Understanding qualification requirements helps you prepare a stronger application for maintaining liquidity through revolving credit. Most lenders evaluate several key factors when considering your business for a credit line.

- Organize financial documentation: Gather recent tax returns, bank statements, profit and loss statements, and balance sheets. Lenders typically want to see at least two years of business financial history to assess your creditworthiness.

- Improve your credit scores: Both personal and business credit scores influence approval odds and terms. Pay down existing debts, correct any reporting errors, and avoid new credit inquiries before applying.

- Demonstrate consistent revenue: Lenders prefer businesses with steady income streams that indicate ability to repay borrowed funds. Prepare documentation showing regular cash flow over recent months or years.

- Prepare a business plan: Even established businesses benefit from having a current business plan that outlines how the credit line supports operational goals and growth strategies.

- Research lender requirements: Different financial institutions have varying criteria for approval. Some focus on revenue levels, others emphasize credit scores, and alternative lenders might consider different factors entirely.

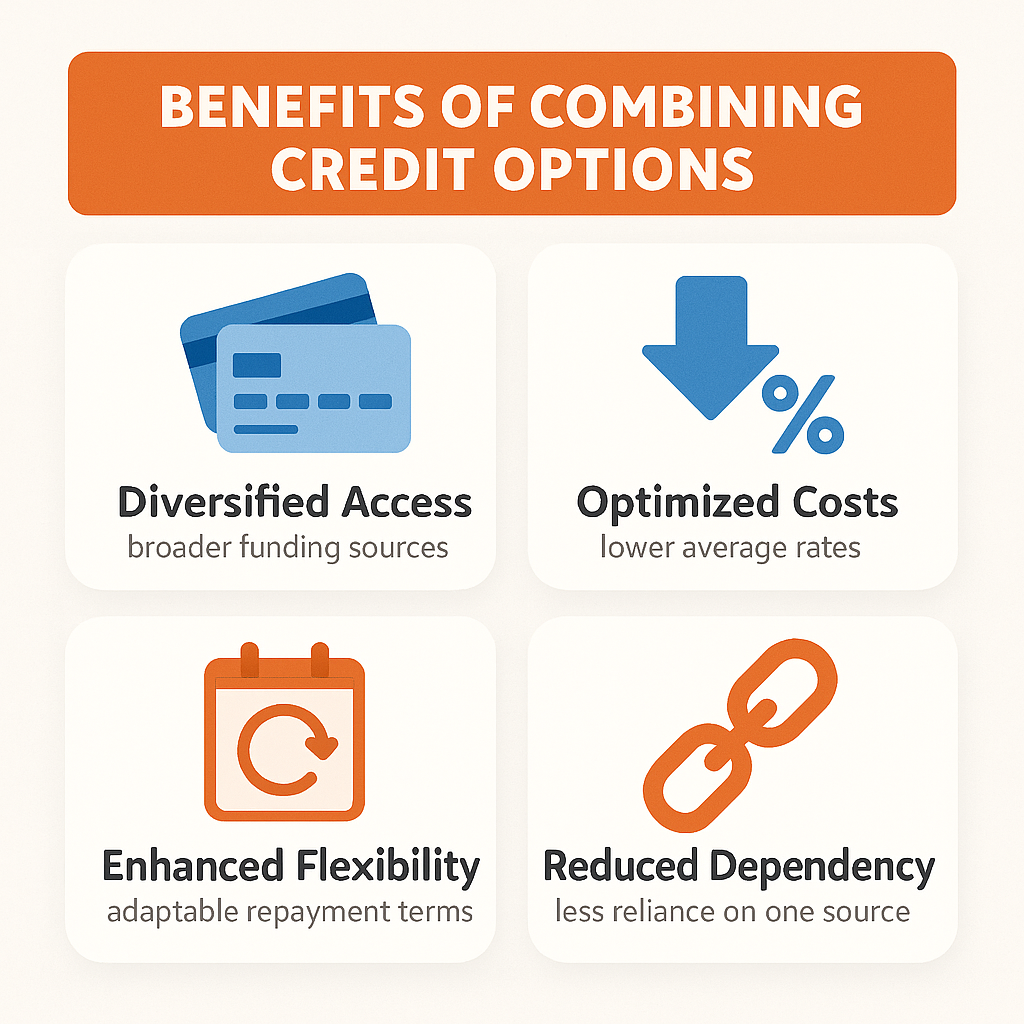

Benefits of Combining Credit Options

Combining LOC with MCA and other financing tools can create a more robust financial strategy for your business. Each option serves different purposes and timing needs in your cash management approach.

- Diversified access to capital: Different funding sources have varying approval processes, repayment terms, and use cases. This diversity ensures you have options when one source might not be available or suitable.

- Optimized costs: Lines of credit typically offer lower costs for longer-term needs, while merchant cash advances might better serve immediate opportunities with quick repayment timelines. Using each tool appropriately can minimize overall financing expenses.

- Enhanced flexibility: Revolving credit benefits include ongoing access to funds, while other options provide lump sums for specific purposes. This combination gives you multiple ways to address various business scenarios.

- Reduced dependency risk: Relying on a single financing source creates vulnerability if that option becomes unavailable. Multiple credit relationships provide backup options and negotiate leverage with lenders.

A business line of credit for cash flexibility represents just one component of a comprehensive financial strategy. When combined with proper planning and potentially other funding options, it can provide the liquidity buffer your business needs to handle unexpected challenges and capitalize on growth opportunities. The key lies in using this tool strategically while maintaining awareness of costs and qualification requirements.

.svg)