.png)

Understanding How to Calculate Line of Credit Interest Charges

Managing a business line of credit effectively starts with understanding exactly how interest charges work. Unlike traditional financing where you pay interest on the full amount, lines of credit typically charge interest only on what you actually use. Learning how to calculate line of credit interest charges can help you make smarter borrowing decisions and potentially save money on financing costs.

The calculation process involves several key factors including your daily interest rate, average daily balance, and the specific terms of your credit agreement. Many business owners find themselves surprised by their monthly statements because they don't fully grasp how these charges accumulate over time.

This guide breaks down the essential components of line of credit interest calculations, giving you the tools to predict your costs and manage your financing more effectively.

Essential Tips for Understanding Daily Interest Calculations

Daily interest calculations form the foundation of how most lines of credit determine your monthly charges. Here are key tips to help you navigate this system:

- Track your daily balances consistently: Your interest charges depend on how much you owe each day, not just your month-end balance. Even small daily fluctuations can impact your total costs over time.

- Understand the daily rate conversion: Most lenders quote annual percentage rates, but they calculate interest daily. The daily rate typically equals your annual rate divided by 365 days, though some lenders may use 360 days.

- Monitor timing of payments and draws: The day you make payments or draw additional funds affects your average daily balance. Strategic timing might help you minimize interest charges during billing cycles.

Key Factors That Influence Your Interest Rate

Several important factors determine the interest rate you'll pay on your line of credit. Understanding these elements can help you work toward better terms:

- Your credit profile and business history: Lenders typically offer better rates to businesses with strong credit scores and established track records. Your personal credit may also factor into the decision for smaller businesses.

- Collateral and security arrangements: Secured lines of credit, backed by business assets or personal guarantees, often come with lower interest rates than unsecured options due to reduced lender risk.

- Market conditions and lender policies: Interest rates fluctuate based on broader economic conditions, and different lenders may have varying risk appetites that affect their pricing structures.

Smart Strategies for Managing Variable Rate Math

Variable rates add complexity to interest calculations since your rate can change over time. Here's how to stay on top of these fluctuations:

- Set up rate change notifications: Many lenders will notify you when rates adjust, but staying proactive about monitoring these changes helps you budget accurately for future payments.

- Calculate costs under different scenarios: Consider how rate increases might affect your monthly expenses, especially if you maintain higher balances during busy seasons or growth periods.

- Review your credit agreement regularly: Understanding when and how your rate can change, including any caps or floors, helps you predict potential cost variations and plan accordingly.

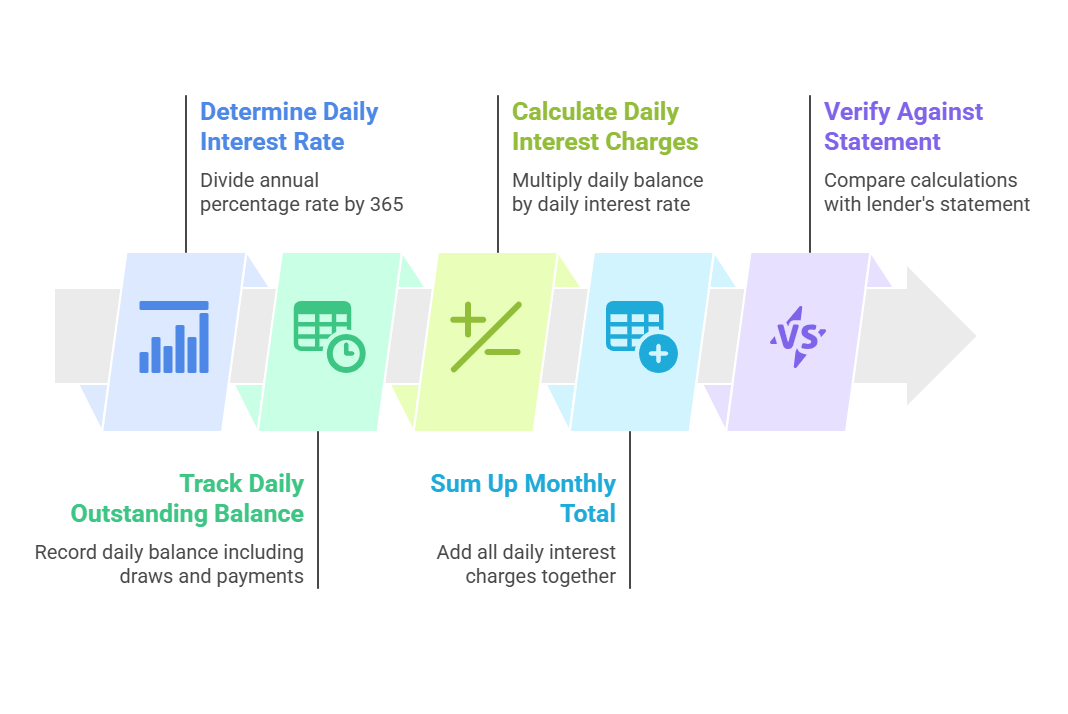

Step-by-Step Interest Calculation Process

Breaking down the calculation process into manageable steps makes it easier to understand your monthly charges:

- Determine your daily interest rate: Divide your annual percentage rate by 365 (or 360, depending on your lender's method) to get your daily rate percentage.

- Track your daily outstanding balance: Record the amount you owe each day during the billing period, including any new draws or payments made.

- Calculate daily interest charges: Multiply each day's balance by your daily interest rate to determine that day's interest cost.

- Sum up the monthly total: Add all daily interest charges together to get your total interest expense for the billing period.

- Verify against your statement: Compare your calculations with your lender's statement to ensure accuracy and address any discrepancies promptly.

Methods for Calculating Average Balance

Some lenders use average balance methods instead of daily calculations, which can affect your total costs:

- Simple average method: Add your beginning and ending balances for the billing period, then divide by two. This works best when your balance remains relatively stable.

- Weighted average daily balance: Calculate the average of all daily balances during the billing cycle, giving more weight to balances held for longer periods.

- Previous balance method: Some lenders may charge interest based on your balance at the end of the previous billing cycle, regardless of payments made during the current period.

- Adjusted balance approach: Interest calculations start from your previous balance minus any payments made, but new purchases or draws may not accrue interest immediately.

Tools and Resources for Managing Credit Costs

Having the right tools can simplify the process of managing your line of credit costs and help you make informed decisions:

- Online calculators and spreadsheet templates: Many financial websites offer free calculators that can help you estimate monthly interest charges based on different balance and rate scenarios.

- Mobile banking and account monitoring: Most lenders provide mobile apps or online portals where you can track daily balances, recent transactions, and interest accruals in real-time.

- Financial planning software: Comprehensive business accounting tools can integrate with your credit accounts to provide automated tracking and forecasting of financing costs.

- Professional financial advice: Working with accountants or financial advisors can help you develop strategies for optimizing your use of credit lines and minimizing overall costs.

Understanding how to calculate line of credit interest charges puts you in control of your financing costs. By mastering the daily interest calculations and average balance methods, you can make more informed decisions about when to draw funds and when to pay down balances.

Remember that variable rate math adds another layer of complexity, but with the right tools and consistent monitoring, you can stay ahead of rate changes and budget accordingly. The key is developing a routine for tracking your daily balances and understanding exactly how your lender calculates charges.

Take time to review your credit agreement terms and don't hesitate to ask your lender questions about their specific calculation methods. With this knowledge, you'll be better positioned to use your line of credit strategically while keeping costs manageable.