.png)

When exploring funding options for your small business, understanding factor rates vs interest rates can make a significant difference in your financial decision-making. These two pricing structures work differently and may impact your business's cash flow and total cost of capital in distinct ways.

Factor Rate Definition and How It Works

A factor rate definition starts with understanding that it's a multiplier used primarily in merchant cash advances rather than a percentage rate. Unlike interest rates that accrue over time, factor rates represent a fixed multiplier applied to the funding amount you receive.

- Simple multiplication structure: Factor rates typically range from 1.1 to 1.5, meaning you might repay $11,000 to $15,000 for every $10,000 received

- No time component: Factor rates don't change based on how quickly you repay the advance, unlike interest rates that compound over time

- Upfront total cost: The total repayment amount is calculated immediately when you receive funding, providing clarity on your financial obligation

- Revenue-based collection: Repayment often occurs through daily or weekly deductions from your business's credit card sales or bank deposits

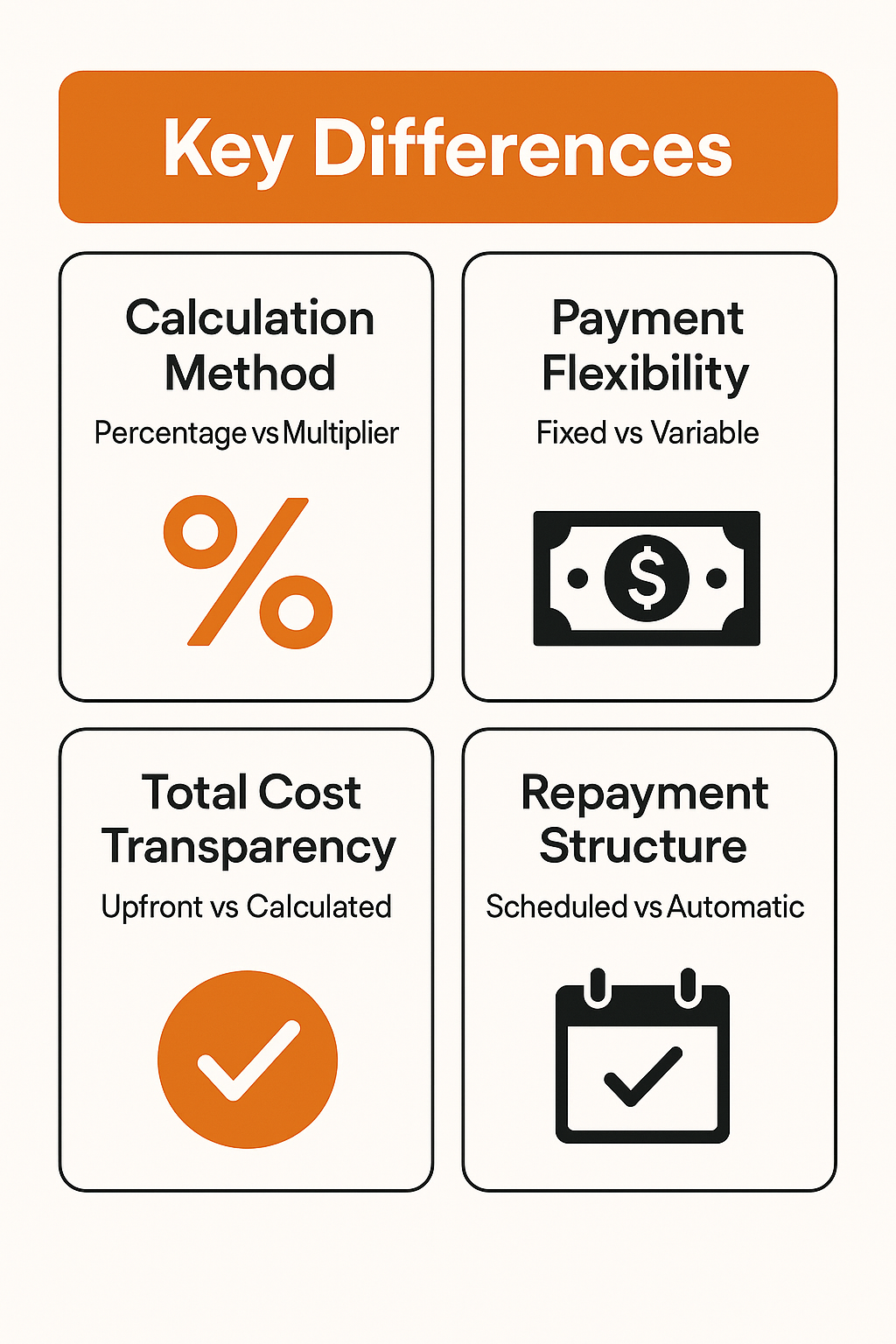

Key Differences Between Factor Rates and Interest Rates

Understanding the fundamental differences between these two pricing models helps you evaluate which funding option might align better with your business needs and cash flow patterns.

- Calculation method: Interest rates calculate cost as a percentage over time periods, while factor rates use a fixed multiplier regardless of repayment timeline

- Payment flexibility: Interest-based loans often have fixed monthly payments, whereas factor rate products may adjust payments based on your daily sales volume

- Total cost transparency: Factor rates show the complete repayment amount upfront, while interest rates require calculations to determine total cost over the loan term

- Repayment structure: Traditional loans with interest rates typically follow scheduled payments, while factor rate advances often collect payments automatically from business revenue

APR Equivalency and Cost Comparison Considerations

Comparing factor rates to traditional interest rates requires understanding APR equivalency, which can help you make more informed funding decisions between different funding options available to your business.

- Converting factor rates: To estimate APR equivalency, you might subtract 1 from the factor rate and divide by the repayment term, though this varies based on payment frequency

- Speed vs cost tradeoff: Factor rate products often provide faster access to capital but may carry higher effective costs compared to traditional interest-based loans

- Cash flow considerations: Businesses with variable revenue might benefit from factor rate products that adjust payments to sales volume, even if the total cost of capital appears higher

- Term length impact: Shorter repayment periods with factor rates might result in higher APR equivalents, while longer traditional loan terms may offer lower overall costs for qualified borrowers

Choosing between factor rates and interest rates depends on your business's specific needs, cash flow patterns, and access to different funding options. Consider factors like speed of funding, repayment flexibility, and total cost when evaluating these financing structures. Understanding these differences can help you select the funding approach that best supports your business goals.