.png)

How to Compare Business Funding Options for Your Growing Business

Understanding how to compare business funding options can make the difference between securing the right financing and getting stuck with unsuitable terms. With the funding landscape evolving rapidly in 2025, business owners face an increasingly complex array of choices, from traditional options to innovative fintech solutions.

The key to making informed decisions lies in understanding the distinct characteristics of each funding type. Whether you're considering merchant cash advances, SBA alternatives, or revenue-based financing, each option comes with unique benefits and requirements that may align differently with your business model and financial situation.

Essential Factors When Evaluating Funding Sources

Evaluating funding sources effectively requires examining several critical factors that could significantly impact your business operations and financial health.

- Cost Structure: Compare the total cost of capital, including fees, factor rates, and interest charges that vary significantly between funding types

- Repayment Terms: Analyze whether you'll make fixed monthly payments, daily remittances based on sales, or percentage-based repayments

- Speed of Access: Consider how quickly you need funds, as some options like MCAs might provide faster access than traditional financing

- Eligibility Requirements: Review credit score minimums, revenue thresholds, and business history requirements that determine qualification

These fundamental factors form the foundation for any funding comparison. The weight you give each factor should align with your business priorities and current financial position.

MCA vs SBA Funding Comparison

When comparing MCA vs SBA options, the differences in structure and accessibility become particularly apparent for business owners.

- Repayment Structure: MCAs typically use daily remittances based on card sales, while SBA programs usually require fixed monthly payments over longer terms

- Credit Requirements: MCAs often accept businesses with less stringent credit requirements, whereas SBA options typically require stronger credit profiles

- Processing Speed: MCAs may provide funding within days, while SBA processes often take weeks or months to complete

- Cost Considerations: SBA programs typically offer lower costs for qualified businesses, while MCAs provide faster access at potentially higher rates

This comparison reveals that each option serves different business funding options and circumstances. Your choice might depend on whether you prioritize speed and accessibility or long-term cost efficiency.

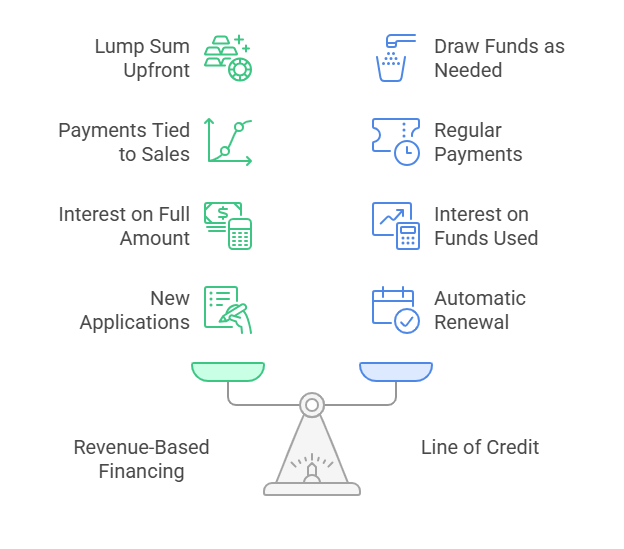

Revenue-Based Financing vs Line of Credit Analysis

The comparison between revenue-based financing vs line of credit reveals two fundamentally different approaches to business funding.

- Usage Flexibility: Lines of credit allow you to draw funds as needed up to your limit, while revenue-based financing typically provides a lump sum upfront

- Repayment Alignment: Revenue-based options tie payments to your actual sales performance, whereas credit lines require regular payments regardless of revenue fluctuations

- Interest Application: Credit lines charge interest only on funds used, while revenue-based financing applies to the full advance amount

- Renewal Process: Credit lines may renew automatically, while revenue-based financing typically requires new applications for additional funding

These structural differences make each option suitable for different business models and cash flow patterns. Companies with seasonal variations might find revenue-based financing more manageable during slower periods.

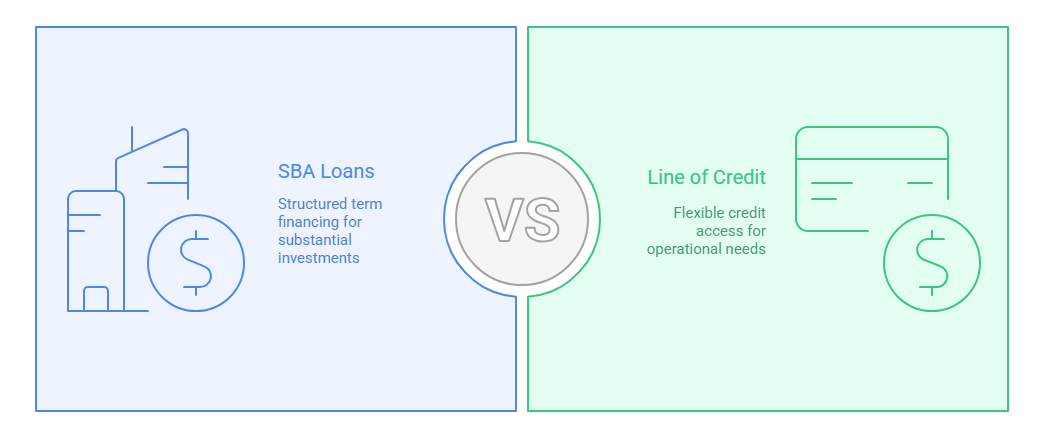

SBA vs Line of Credit Considerations

Understanding SBA vs line of credit differences helps businesses choose between structured term financing and flexible credit access.

- Funding Amount: SBA programs often provide larger funding amounts for substantial business investments, while credit lines offer smaller, flexible access

- Application Process: SBA applications typically require extensive documentation and longer approval times, whereas credit lines may have streamlined processes

- Use Restrictions: SBA funds often come with specific use requirements, while credit lines provide more flexibility in how you deploy capital

- Long-term Impact: SBA financing builds business credit history through structured repayment, while credit lines demonstrate ongoing creditworthiness through responsible usage

The choice between these options often comes down to whether you need substantial capital for specific projects or prefer ongoing access to smaller amounts for operational flexibility.

Step-by-Step Funding Comparison Process

Following a systematic approach ensures you evaluate funding options thoroughly and make informed decisions for your business.

- Assess Your Funding Needs: Determine the exact amount needed, intended use, and timeline for accessing funds to narrow your options effectively

- Review Your Financial Profile: Analyze your credit score, revenue history, and business documentation to understand which options you might qualify for

- Calculate Total Costs: Compare the complete cost of each option, including fees, rates, and any additional charges over the full term

- Evaluate Terms and Flexibility: Consider repayment schedules, prepayment options, and how each structure aligns with your cash flow patterns

- Research Provider Reputation: Investigate lender reviews, industry standing, and customer service quality to ensure reliable partnership

This methodical approach helps prevent overlooking crucial details that could impact your decision. Taking time for thorough evaluation typically leads to better funding outcomes and stronger business relationships.

Common Eligibility Requirements Across Funding Types

Understanding eligibility criteria helps you identify which funding options might be accessible and prepare appropriate documentation for applications.

- Credit Score Thresholds: Requirements typically range from 500+ for some MCAs to 680+ for traditional options, with each lender setting specific minimums

- Revenue Requirements: Most lenders require minimum monthly or annual revenue, often ranging from $10,000 to $100,000+ depending on the funding type

- Business Age Criteria: Time in business requirements vary from 3-6 months for alternative options to 2+ years for traditional financing

- Documentation Standards: Prepare bank statements, tax returns, and financial statements, with requirements varying by lender and funding amount

- Industry Considerations: Some lenders restrict certain industries or require additional documentation for high-risk business types

Meeting eligibility requirements doesn't guarantee approval, but understanding these criteria helps you focus on realistic options and prepare stronger applications. When comparing different business funding options, consider working with financial advisors if you're uncertain about qualification.

Making Your Final Funding Decision

After thorough comparison and evaluation, the final decision should align with both your immediate needs and long-term business strategy. Consider not just the terms and costs, but how each option supports your growth objectives and operational requirements. The best fit for your business typically balances accessibility, cost efficiency, and strategic fit with your business model.

Learning how to compare business funding options effectively empowers you to make decisions that support your business growth while managing financial risk appropriately. Remember that the funding landscape continues evolving, with new options emerging regularly. Stay informed about available alternatives and reassess your funding strategy as your business grows and market conditions change.

The right funding partner should understand your business needs and provide transparent terms that align with your goals. Take time to evaluate options thoroughly, ask detailed questions, and choose funding that positions your business for sustainable success.