.png)

When seeking business financing, one of the most important decisions you'll face is choosing between collateral vs unsecured business loans. This choice affects everything from your interest rates to approval speed and the risk to your business assets. Understanding these fundamental differences helps you select the financing option that aligns with your business needs and risk tolerance.

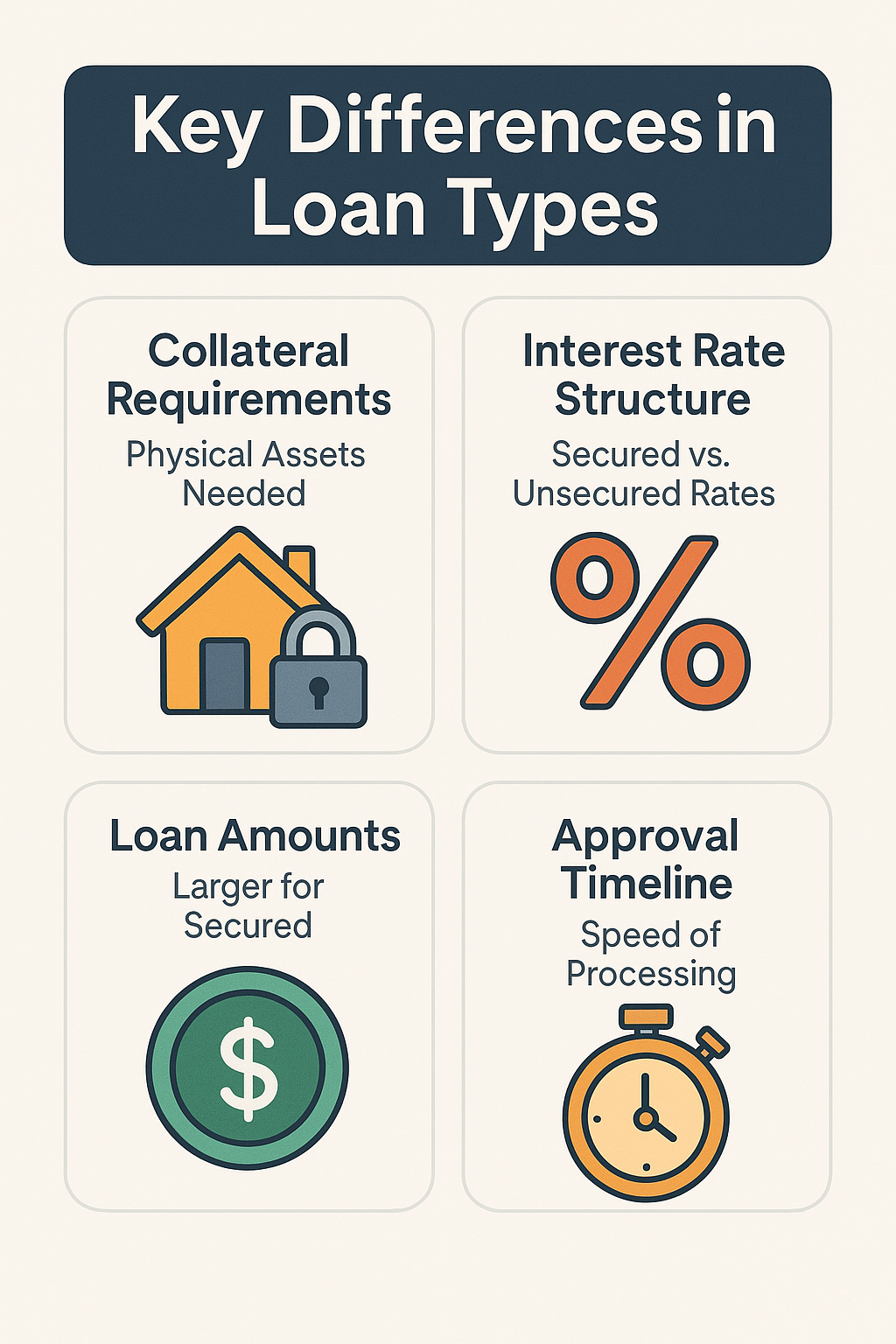

Key Differences Between Secured and Unsecured Business Loans

The primary distinction in collateral vs unsecured business loans lies in what you're required to pledge as security. These differences create cascading effects on loan terms, approval requirements, and your financial obligations.

- Collateral Requirements: Secured loans require physical assets like equipment, inventory, or real estate as backing, while unsecured loans rely solely on your creditworthiness and business performance

- Interest Rate Structure: Secured loans typically offer lower interest rates because lenders face reduced risk, whereas unsecured loans carry higher rates to compensate for increased lender risk

- Loan Amounts: Asset based lending often allows for larger loan amounts since the collateral provides security, while unsecured loans may have lower limits based on cash flow and credit scores

- Approval Timeline: Unsecured loans frequently process faster due to simplified documentation, while secured loans require asset valuations and additional paperwork

Steps to Evaluate Which Loan Type Suits Your Business

Determining the right choice in collateral vs unsecured business loans requires a systematic approach to assess your specific circumstances and financing goals.

- Assess Your Available Assets: Inventory valuable business assets like equipment, real estate, or accounts receivable that could serve as collateral for asset based lending options

- Calculate Interest Differential Impact: Compare the total cost of borrowing between secured and unsecured options, factoring in the interest rate difference over your intended loan term

- Evaluate Your Risk Tolerance: Consider whether you're comfortable pledging business assets against the loan or prefer keeping assets unencumbered despite higher costs

- Determine Timeline Requirements: Match your funding urgency with typical approval timeframes, remembering that unsecured loans often process more quickly

Risk Tradeoffs in Secured vs Unsecured Financing

Understanding risk tradeoffs helps you make informed decisions about collateral vs unsecured business loans. Secured loans put your pledged assets at risk if you default, but they often come with more favorable terms and lower monthly payments. The asset based lending approach means your equipment, inventory, or other collateral could be seized if you fail to meet payment obligations.

Unsecured loans eliminate the risk of losing specific business assets, but they typically require personal guarantees from business owners. These personal guarantees can put your personal assets and credit at stake. Additionally, unsecured loans often have stricter qualification requirements and higher interest rates, which increases your overall borrowing costs and monthly cash flow impact.

Ideal Use Cases for Each Loan Type

Choosing between collateral vs unsecured business loans depends heavily on your specific business situation and financing needs. Secured loans work well when you need substantial funding for equipment purchases, real estate acquisitions, or major expansions where you have valuable assets to pledge. The lower interest rates make them particularly attractive for long term investments where the interest differential significantly impacts total costs.

Unsecured loans excel in situations requiring quick access to capital, such as covering seasonal cash flow gaps, taking advantage of time sensitive opportunities, or funding working capital needs. They're also preferred when you want to preserve asset flexibility or lack sufficient collateral for secured financing. The faster approval process makes unsecured options ideal when speed matters more than minimizing borrowing costs.

The choice between collateral vs unsecured business loans ultimately depends on your risk tolerance, available assets, and specific financing needs. Secured loans offer lower costs but require asset pledging, while unsecured loans provide flexibility at higher rates. Consider your business timeline, asset base, and comfort level with risk when making this important financing decision.

.svg)