.png)

Running a small business means facing uncertainty every day, from market fluctuations to supply chain disruptions. That's why developing comprehensive risk management strategies for small businesses has become more critical than ever. These protective measures can mean the difference between weathering a storm and closing your doors permanently.

Smart business owners understand that risk management isn't just about preventing disasters. It's about creating a foundation that allows your company to adapt, grow, and thrive despite challenges. Whether you're dealing with cash flow concerns, operational disruptions, or competitive pressures, having the right strategies in place helps you stay focused on what matters most: serving your customers and building your business.

Building Your Risk Assessment Foundation

Building your risk assessment foundation starts with understanding what could potentially impact your business operations. The first step involves conducting a thorough review of your current processes, identifying areas where disruptions might occur. This systematic approach helps you prioritize which risks need immediate attention and which ones you can address over time.

- Document all business processes: Create detailed workflows that outline how your business operates on a daily basis. This documentation helps you spot potential weak points where disruptions could cause significant problems.

- Categorize risks by impact level: Not all risks carry the same weight for your business success. Focus your energy on addressing high-impact threats first, while keeping medium and low-impact risks on your monitoring list.

- Review historical data: Look at past challenges your business has faced to identify patterns. Understanding what went wrong before often provides valuable insights into what might go wrong again.

Smart Insurance Planning Approaches

Smart insurance planning approaches protect your business from financial devastation when unexpected events occur. Insurance planning serves as your safety net, covering everything from property damage to liability claims that could otherwise bankrupt a small operation. The key lies in understanding which coverage types align with your specific business model and risk profile.

- Evaluate property and liability needs: Consider what physical assets need protection and what liability exposures your business activities create. A retail store faces different risks than a consulting firm, so your coverage should reflect those differences.

- Consider business interruption coverage: This protection helps replace lost income when disasters force you to temporarily close operations. It might cover rent, payroll, and other ongoing expenses while you get back on your feet.

- Review coverage annually: Your insurance needs change as your business grows and evolves. What protected you last year might leave gaps in coverage today, especially if you've added new services or expanded operations.

Effective Supplier Diversification Methods

Effective supplier diversification methods prevent your business from becoming overly dependent on any single source for critical materials or services. When you rely too heavily on one supplier, their problems automatically become your problems. Creating a network of reliable alternatives ensures you can maintain operations even when disruptions occur.

- Identify backup suppliers for critical items: Research and establish relationships with secondary suppliers before you need them. Having these connections already in place saves precious time when your primary supplier faces difficulties.

- Negotiate flexible terms: Work with suppliers to create agreements that allow for quantity adjustments during busy or slow periods. This flexibility helps you manage costs while maintaining adequate inventory levels.

- Monitor supplier financial health: Keep an eye on your suppliers' business conditions through trade publications and industry networks. Early warning signs might give you time to find alternatives before supply disruptions occur.

Contract Review Best Practices

Contract review best practices help you avoid costly disputes and ensure clear expectations with customers, suppliers, and service providers. Well-structured contracts often serve as your first line of defense against misunderstandings that could escalate into expensive legal battles or damaged business relationships.

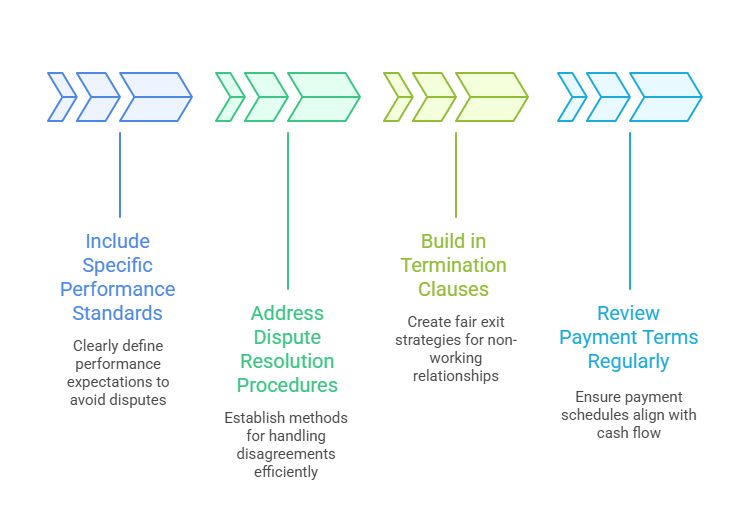

- Include specific performance standards: Clearly define what constitutes acceptable performance, delivery timelines, and quality expectations. Vague language creates opportunities for disputes that could have been prevented with better documentation.

- Address dispute resolution procedures: Establish how you'll handle disagreements before they arise. Mediation or arbitration clauses might save you thousands in legal fees compared to traditional litigation.

- Build in termination clauses: Create fair but firm exit strategies for when relationships aren't working out. These provisions protect both parties and provide clear paths forward when changes become necessary.

- Review payment terms regularly: Ensure your payment schedules align with your cash flow patterns. Extended payment terms might seem attractive but could create problems if your own customers pay slowly.

Liquidity Protection Strategies

Liquidity protection strategies ensure your business maintains adequate cash flow to handle unexpected expenses or temporary revenue drops. Cash flow problems kill more small businesses than almost any other single factor, making liquid reserves essential for long-term survival and growth opportunities.

- Maintain emergency cash reserves: Set aside funds equal to three to six months of operating expenses in easily accessible accounts. This cushion provides breathing room when revenue temporarily declines or unexpected costs arise.

- Establish credit facilities before you need them: Apply for credit lines during strong financial periods rather than waiting until cash becomes tight. Lenders prefer working with businesses that demonstrate forward-thinking financial management.

- Monitor accounts receivable closely: Implement systems to track when customers should pay and follow up promptly on overdue accounts. Faster collections improve your cash position and reduce the risk of bad debts.

- Consider invoice factoring options: When immediate cash flow becomes critical, factoring allows you to convert outstanding invoices into immediate working capital, though this comes with costs that need careful evaluation.

Technology and Data Security Measures

Technology and data security measures protect your business from cyber threats that could compromise customer information, disrupt operations, or damage your reputation. Small businesses often become targets because they typically have fewer security resources than larger companies, making robust protection essential for maintaining customer trust and operational continuity.

- Implement regular data backups: Automated backup systems ensure you can recover critical information if hardware fails or cyber attacks occur. Store backups in multiple locations, including cloud-based services, for maximum protection against various disaster scenarios.

- Train employees on security protocols: Human error causes many security breaches, so education becomes your first line of defense. Regular training helps staff recognize phishing attempts, use strong passwords, and follow proper procedures for handling sensitive information.

- Update software systems regularly: Keep operating systems, applications, and security software current with the latest patches and updates. Cybercriminals often exploit known vulnerabilities in outdated software to gain unauthorized access to business systems.

- Monitor financial accounts daily: Regular account reviews help you spot unauthorized transactions quickly, potentially limiting damage from fraud or theft. Early detection often makes the difference between minor inconvenience and major financial loss.

Implementing comprehensive risk management strategies for small businesses requires ongoing attention and regular updates as your company evolves. The investment in insurance planning, supplier diversification, contract reviews, and liquidity protection pays dividends when unexpected challenges arise. Remember that risk management isn't a one-time project but rather an ongoing process that strengthens your business foundation.

Start with the strategies that address your most significant vulnerabilities, then gradually build out your protection systems over time. Small improvements in risk management often yield substantial benefits in business stability and growth potential. Your future self will thank you for taking these protective steps today, especially when you're able to navigate challenges that might have otherwise threatened your business survival.