.png)

Getting approved for business funding often feels like a mystery. You submit your application and wait, wondering what criteria lenders use to make their decisions. Understanding how funding approvals are determined can significantly improve your chances of success and help you prepare stronger applications.

Modern funding providers evaluate several key factors when reviewing applications, from business revenue patterns to credit assessments and documentation quality. The good news is that many alternative funding options, like merchant cash advances, have streamlined their approval processes to focus on what matters most: your business's actual performance and cash flow.

Common Questions About Funding Approval Processes

Q: How quickly can funding approvals be processed?

Many alternative funding providers, particularly merchant cash advance companies, can approve and disburse funds within 1-3 business days. This speed comes from streamlined processes that focus on cash flow analysis rather than extensive paperwork.

Q: What's the most important factor in approval decisions?

Business revenue consistency tends to be the primary consideration for most alternative funding providers. They want to see steady sales patterns that demonstrate your ability to handle repayment obligations.

Q: Do I need perfect credit for approval?

Not necessarily. Many funding options involve minimal underwriting requirements and focus more on your business's current performance than historical credit issues.

Key Revenue Assessment Criteria

Revenue assessment criteria form the backbone of most funding decisions. Lenders examine multiple aspects of your business revenue to gauge repayment capability and overall financial health.

- Monthly sales consistency: Providers typically look for steady revenue patterns over the past 6-12 months, avoiding businesses with extreme fluctuations that might indicate instability.

- Seasonal trends analysis: Understanding your business's natural cycles helps lenders determine appropriate funding amounts and repayment structures that align with your cash flow.

- Growth trajectory evaluation: Businesses showing upward revenue trends often receive more favorable consideration, as growth indicates strong market demand and management capability.

- Industry benchmarking: Your revenue performance gets compared against similar businesses in your sector to ensure realistic expectations and appropriate risk assessment.

Credit Assessment Components

Credit assessment involves examining both personal and business credit profiles, though the weight given to each varies significantly between funding types and providers.

- Personal credit score impact: While important, many alternative funding providers may approve businesses with less-than-perfect personal credit if other factors compensate for the deficiency.

- Business credit history review: Established businesses with positive trade references and payment histories typically receive better terms and higher approval rates.

- Debt-to-income ratios: Lenders evaluate existing debt obligations against current income to ensure new funding won't overextend your business financially.

- Payment behavior patterns: Consistent on-time payments to vendors, utilities, and other creditors demonstrate reliability that funding providers value highly.

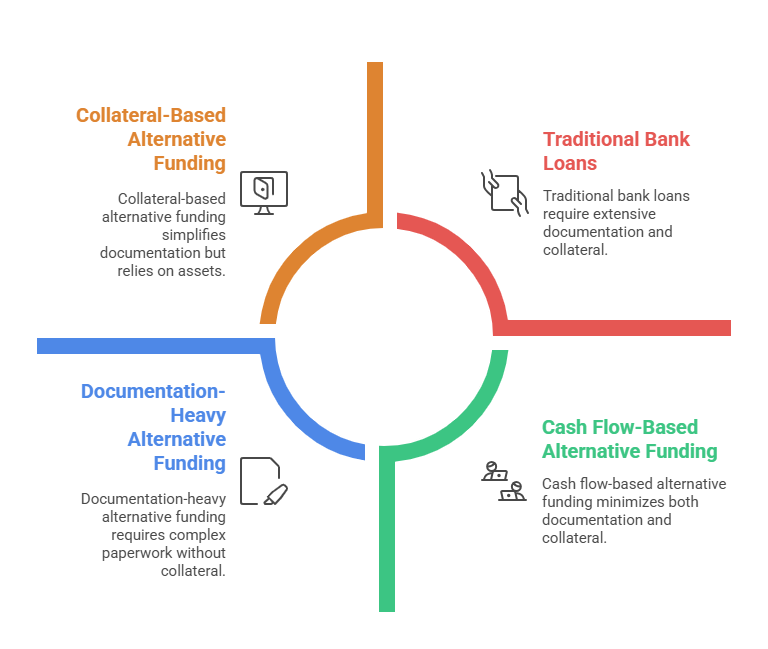

Documentation Review Requirements

Documentation review requirements vary significantly between traditional and alternative funding sources, with many modern providers simplifying their requirements to speed up the approval process.

- Financial statements accuracy: Bank statements, profit and loss statements, and cash flow reports must be current, complete, and accurately reflect your business operations.

- Tax return verification: Recent business tax returns help verify reported income and provide insight into your business's financial management practices.

- Legal compliance documentation: Business licenses, registrations, and permits demonstrate that your operation meets regulatory requirements in your industry and location.

- Collateral documentation: Some funding types may require asset documentation, though many alternative options focus on cash flow rather than collateral requirements.

Steps to Improve Your Approval Chances

Taking proactive steps to strengthen your funding application can significantly increase approval chances and potentially secure better terms for your business.

- Organize financial records systematically: Maintain accurate, up-to-date financial documentation that clearly shows your business's performance trends and current financial position.

- Build consistent revenue patterns: Focus on creating steady sales streams rather than relying on sporadic large transactions that might appear unstable to lenders.

- Address credit issues proactively: Work on improving both personal and business credit scores by paying bills on time and reducing outstanding debt balances.

- Choose appropriate funding amounts: Request funding amounts that align realistically with your revenue and repayment capacity rather than maximizing the request.

- Research provider requirements: Different funding sources have varying criteria, so matching your application to providers whose requirements fit your business profile increases success rates.

Timeline Expectations for Different Funding Types

Understanding typical approval timelines helps you plan better and set realistic expectations for when funding might become available for your business needs.

- Merchant cash advances: These typically offer the fastest approval process, with decisions often made within 24-48 hours and funds available within 1-3 business days of approval.

- Revenue-based financing: Similar to merchant cash advances in speed, these funding options usually complete their approval process within 2-5 business days depending on documentation completeness.

- Traditional term financing: These options generally require more extensive review periods, with approval processes potentially taking 1-4 weeks due to thorough documentation requirements.

- Secured funding options: When collateral is involved, additional appraisal and verification steps may extend the timeline to 2-6 weeks for final approval and funding.

Understanding how funding approvals are determined puts you in a stronger position to secure the capital your business needs. The key factors, revenue consistency, credit assessment quality, thorough documentation, and choosing the right funding type, all work together to influence approval decisions.

Remember that different funding providers emphasize different criteria. While traditional lenders might focus heavily on credit scores and collateral, alternative funding sources often prioritize cash flow and revenue patterns. This variety means that even if one option doesn't work out, other funding paths might be more suitable for your business situation.

The most successful funding applications come from businesses that have taken time to understand what providers are looking for and have prepared accordingly. By focusing on these key areas and maintaining good financial practices, you'll be well-positioned to secure funding when opportunities arise.