.png)

Understanding how merchant receivables are calculated might be one of the most important skills for any business owner considering alternative financing. When you're exploring merchant cash advances, the calculation process directly impacts your repayment obligations and cash flow planning. These calculations involve several key factors that determine how much you'll pay back and when those payments will be collected from your daily sales.

The calculation process combines your advance amount with factor rates and fees, creating a total repayment figure that gets collected through a percentage of your daily credit card transactions. This systematic approach helps lenders assess risk while providing businesses with predictable repayment structures based on actual revenue performance.

Best Practices for Understanding Receivable Calculations

Best practices for understanding receivable calculations can help you navigate the merchant cash advance process more effectively. Following these guidelines typically leads to better financial planning and more accurate revenue forecasting.

- Use MCA calculators to estimate your total repayment amount before committing to any advance, as these tools help you understand potential financial obligations

- Review all factor rates carefully since they directly impact how merchant receivables are calculated and determine your total cost

- Analyze your daily sales patterns to ensure the repayment percentage aligns with your typical revenue flow

- Document all fees and terms in writing to avoid surprises during the repayment process

- Compare multiple offers using consistent calculation methods to identify the most suitable financing option

Common Mistakes in Receivable Calculation Analysis

Common mistakes in receivable calculation analysis can lead to financial strain and unexpected costs. Avoiding these pitfalls helps ensure more accurate repayment estimation and better cash flow management.

- Don't ignore additional fees beyond the factor rate, as these costs significantly affect your total repayment amount

- Don't assume all calculation methods are identical across different providers, since terms and structures may vary considerably

- Don't base projections solely on peak sales periods without considering seasonal fluctuations in your revenue

- Don't overlook the impact of daily collection percentages on your working capital during slower business periods

- Don't skip the verification process for calculation accuracy, as errors can compound throughout the repayment term

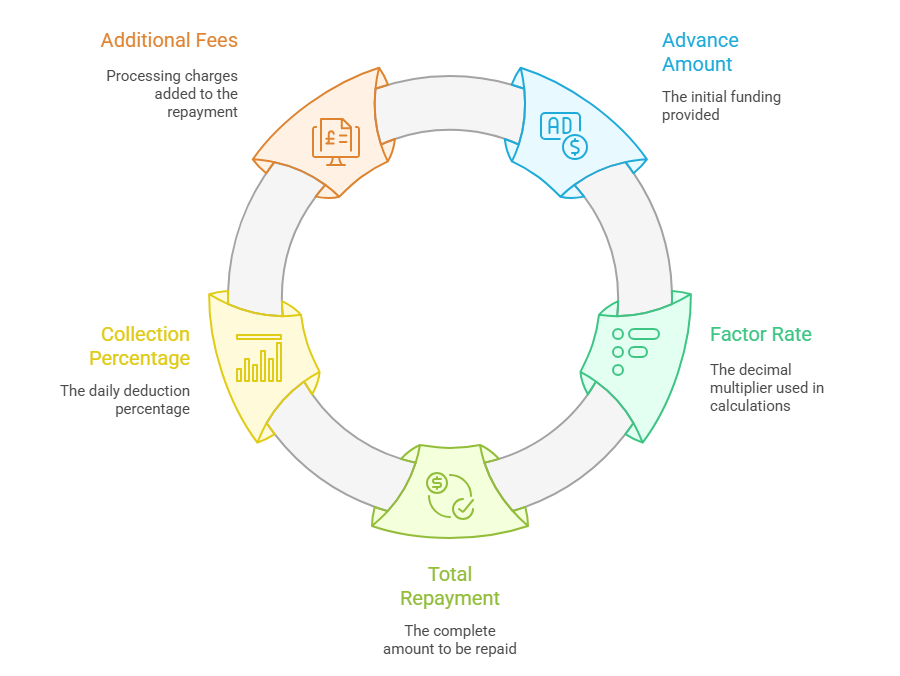

Key Components in Merchant Receivable Calculations

Key components in merchant receivable calculations form the foundation for determining your repayment obligations. Understanding these elements helps you perform better sales analysis and underwriting evaluation.

- Advance Amount: The principal funding you receive upfront, which serves as the base for all subsequent calculations and determines the scale of your repayment obligations.

- Factor Rate: A decimal multiplier typically ranging from 1.1 to 1.5 that gets multiplied by your advance amount to determine total repayment cost.

- Total Repayment Sum: The result of multiplying your advance amount by the factor rate, representing the complete amount you'll pay back over the term.

- Collection Percentage: The daily percentage of credit card sales that gets automatically deducted to satisfy your repayment obligation until the total sum is collected.

- Additional Fees: Processing charges, origination fees, or administrative costs that may be added to your total repayment calculation depending on the provider's terms.

Revenue Forecasting Methods for Accurate Projections

Revenue forecasting methods for accurate projections help you predict how receivable collections will impact your daily operations. These approaches support better repayment estimation and financial planning.

- Historical Sales Analysis: Review 12-24 months of transaction data to identify patterns, seasonal trends, and average daily sales volumes that influence collection timing.

- Seasonal Adjustment Calculations: Factor in predictable fluctuations like holiday peaks or summer slowdowns that affect how quickly your receivables get collected through daily sales.

- Growth Rate Projections: Consider anticipated business expansion or contraction that might alter your revenue stream and subsequent repayment schedule during the advance term.

- Industry Benchmark Comparison: Compare your sales patterns against similar businesses to validate forecasting assumptions and identify potential revenue optimization opportunities.

Underwriting Factors That Influence Calculation Terms

Underwriting factors that influence calculation terms play a crucial role in determining how merchant receivables are calculated for your specific situation. Lenders evaluate these criteria to assess risk and establish appropriate terms.

- Credit Card Processing Volume: Higher monthly processing amounts typically lead to more favorable factor rates since they demonstrate consistent revenue streams for receivable collection.

- Business Operating History: Established businesses with longer track records often receive better calculation terms due to proven stability and predictable sales patterns.

- Industry Risk Assessment: Certain business types may face different factor rates based on industry-specific risk profiles and typical receivable collection patterns.

- Cash Flow Consistency: Regular, predictable revenue streams influence the collection percentage and repayment timeline calculations offered by potential funding providers.

Mastering how merchant receivables are calculated empowers you to make informed financing decisions that align with your business goals. The calculation process involves multiple components working together, from factor rates and advance amounts to daily collection percentages and additional fees. By understanding these elements, you can better predict repayment obligations and plan your cash flow accordingly.

Remember that accurate revenue forecasting and thorough sales analysis form the backbone of successful merchant cash advance management. Take time to review your historical data, consider seasonal variations, and use available calculation tools to estimate your obligations before committing to any advance.

When you're ready to explore merchant cash advance options, having this knowledge helps you evaluate offers more effectively and choose terms that support your business operations rather than strain them.