.png)

Small businesses often struggle to maintain steady cash flow while pursuing growth opportunities. SBA working capital options for small businesses offer a solution through government-backed financing programs that provide lower interest rates and flexible terms. With recent changes to SBA lending programs in 2025, understanding your options has become more important than ever.

Understanding SBA Working Capital Programs

SBA working capital programs help small businesses bridge cash flow gaps and fund day-to-day operations through government-backed financing. The 7(a) program stands as the SBA's most popular option, offering various loan types designed to meet different business needs.

Working capital from SBA programs typically provides more favorable terms than traditional bank financing. These programs may offer lower down payments, extended repayment periods, and competitive interest rates that can make a significant difference in your monthly cash flow management.

Recent regulatory changes in 2025 have restored previous underwriting criteria, which could affect approval processes and terms. Business owners should understand these modifications when planning their funding strategy and preparing applications.

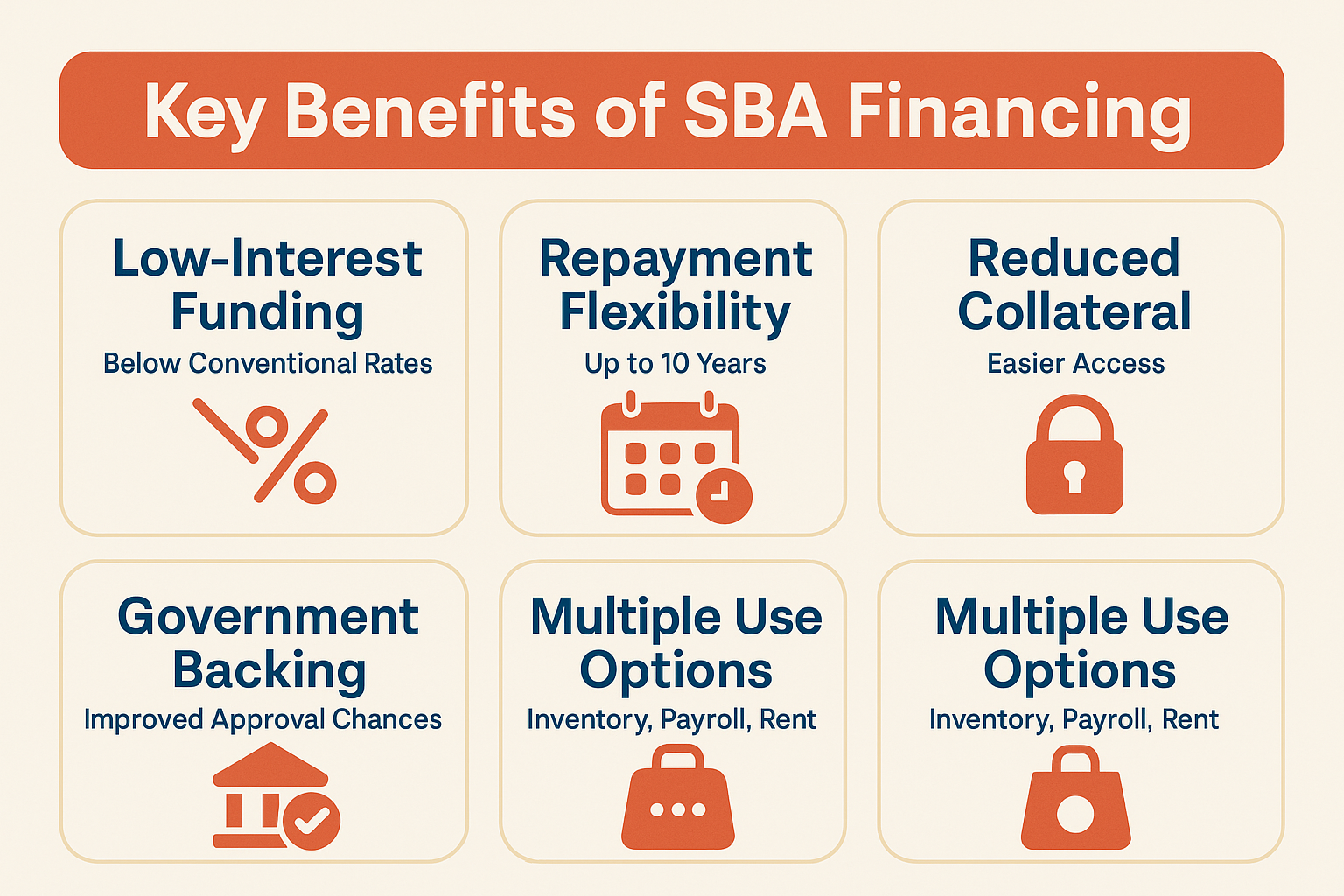

Key Benefits of SBA Working Capital Financing

SBA working capital options offer several advantages that make them attractive to small business owners seeking cash flow stabilization:

- Low-interest funding with rates typically below conventional business financing options

- Repayment flexibility through extended terms that can span up to 10 years for working capital needs

- Reduced collateral requirements compared to traditional bank financing, making access easier for qualifying businesses

- Government backing that reduces lender risk and may improve approval chances for eligible applicants

- Multiple use options including inventory purchases, payroll, rent, and other operational expenses

Steps to Secure SBA Working Capital

Securing SBA working capital requires careful preparation and understanding of the application process:

- Assess your eligibility based on current SBA size standards and business requirements, keeping in mind recent regulatory adjustments

- Prepare comprehensive financial documentation including tax returns, financial statements, and cash flow projections that demonstrate your need

- Choose the right 7(a) loan type from available options that best align with your specific working capital requirements

- Work with an approved SBA lender who understands the current underwriting criteria and can guide you through the process

- Submit a complete application with all required documentation to avoid delays in the approval process

Making the Most of Your SBA Funding

Once approved, strategic use of your SBA working capital can maximize its impact on your business operations. Focus on cash flow stabilization activities that generate revenue or reduce operational costs. Monitor your spending carefully and maintain detailed records to ensure compliance with SBA requirements while building a strong foundation for future growth.

SBA working capital options provide valuable financing solutions for small businesses seeking growth and stability. With recent program changes and potential increases in loan limits, now may be an opportune time to explore these government-backed funding options. Consider consulting with experienced lenders to determine which SBA program best fits your business needs and cash flow objectives.

.svg)