.png)

Securing business financing requires more than just a good business idea. Lenders evaluate specific criteria before approving loan applications, and understanding business loan requirements can significantly improve your chances of success. Recent changes to SBA guidelines and traditional lending standards have shifted what financial institutions expect from borrowers. Small business owners who prepare thoroughly and meet these benchmarks position themselves for better terms and faster approval processes.

Credit Score Standards and Financial Metrics Lenders Require

Understanding what lenders look for in small business loans starts with credit requirements. Most traditional lenders expect personal credit scores above 690, while SBA loans have recently increased their minimum thresholds. Your credit profile demonstrates your ability to manage debt responsibly and directly impacts loan terms and interest rates.

Beyond credit scores, lenders examine your business's financial health through several key metrics. Cash flow statements reveal whether your business generates sufficient income to cover loan payments. Debt-to-income ratios show how much existing debt you carry relative to your earnings. Revenue trends over the past two years indicate business stability and growth potential.

Profitability margins matter significantly in loan decisions. Lenders want to see consistent profit generation, not just high revenue numbers. They also evaluate your industry's risk profile and seasonal fluctuations that might affect repayment ability. Businesses operating for at least two years typically have better approval odds since they can demonstrate established financial patterns.

Essential Documents Needed for Business Loan Applications

The documents needed for business loan applications vary by lender and loan type, but certain paperwork remains standard across most applications. Financial statements form the foundation of your application package. These include profit and loss statements, balance sheets, and cash flow projections for at least the past two years.

Tax returns provide independent verification of your reported income and business performance. Lenders typically request both personal and business tax returns for the previous two to three years. Bank statements demonstrate your cash management practices and account activity patterns. Most lenders want to see three to six months of recent statements.

Business documentation proves your company's legitimacy and structure. This includes business licenses, articles of incorporation, operating agreements, and any franchise agreements. Personal financial statements reveal your individual financial position, which matters since many small business loans require personal guarantees. Some lenders may request additional documentation like customer contracts, supplier agreements, or lease documents depending on your business type.

SBA Loan Requirements and Recent Changes

Tip 1: Recent SBA guideline changes include stricter underwriting standards and higher minimum credit scores. Businesses should review their credit profiles well before applying and address any issues that might affect qualification.

Tip 2: The maximum loan cap for certain SBA programs has been reduced to $350,000, requiring businesses to plan their financing needs more precisely. Consider whether you need additional funding sources to meet your capital requirements.

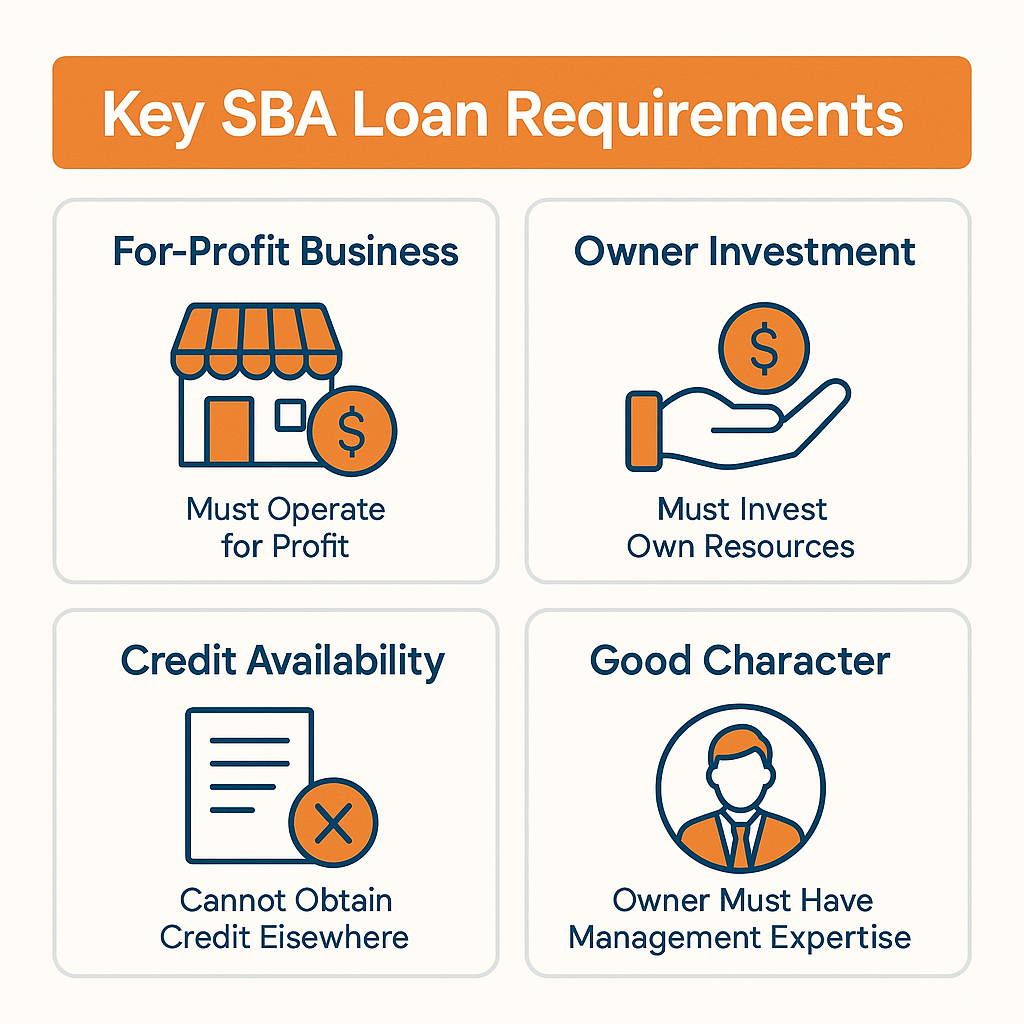

SBA loans require businesses to operate for profit and meet specific size standards defined by the administration. Your business must demonstrate that you've invested your own time and money before seeking SBA financing.

Key SBA 7(a) loan requirements include:

- Business must be for-profit and meet SBA size standards

- Owner must have invested their own resources

- Business must not be able to obtain credit elsewhere

- Owner must be of good character with management expertise

- Business must operate primarily in the United States

Understanding business loan requirements gives you a strategic advantage in the application process. Strong credit profiles, comprehensive documentation, and alignment with current lending standards significantly improve your approval chances. While requirements have become more stringent, particularly for SBA loans, preparation and professional presentation of your financial position can overcome many obstacles. Take time to review your credit, organize required documents, and ensure your business meets all eligibility criteria before submitting applications. This preparation not only increases approval odds but often results in better loan terms and interest rates for your business.