.png)

When it comes to securing business funding, most owners focus on approval speed and funding amounts. However, understanding funding terms most businesses overlook can mean the difference between sustainable growth and unexpected financial strain. The fine print in funding agreements often contains provisions that might significantly impact your cash flow, repayment obligations, and long-term financial health.

Many merchants rush through the funding process without adequately preparing or examining the full scope of their agreements. This oversight can lead to unfavorable terms, higher costs, and contractual obligations that weren't immediately apparent. By learning what to look for in your funding documents, you'll be better positioned to negotiate terms that work for your business rather than against it.

In this article, we'll explore the commonly overlooked aspects of business funding agreements, from hidden contract clauses to repayment structures that could affect your operations. Whether you're considering your first funding arrangement or looking to refinance existing obligations, this guide will help you navigate the process with greater confidence and awareness.

Common Contract Clauses That Create Hidden Risks

Common contract clauses that create hidden risks are often buried in funding agreements where business owners least expect them. These provisions can shift financial burdens and operational control in ways that aren't immediately obvious during initial review.

- Automatic renewal provisions: Many funding contracts include clauses that automatically extend your agreement unless you provide notice within a specific timeframe. Missing this window could lock you into another term with the same rates and conditions, even if better options become available.

- Unilateral modification rights: Some agreements give the funding provider the right to change certain terms with minimal notice. This might include adjusting fees, changing reporting requirements, or modifying payment schedules in ways that could strain your operations.

- Cross-default clauses: These provisions mean that if you default on any other financial obligation, it could trigger a default on your funding agreement as well. This creates a domino effect that might put multiple aspects of your business at risk simultaneously.

- Personal guarantee requirements: While often discussed upfront, the full implications of personal guarantees can be underestimated. These clauses may extend your personal liability beyond what you initially understood, potentially putting personal assets at risk if business circumstances change.

Being vigilant about these contract elements helps ensure you're entering agreements with full awareness of the obligations you're accepting. Taking time to identify and understand these clauses before signing can prevent long-term complications that might otherwise catch you off-guard.

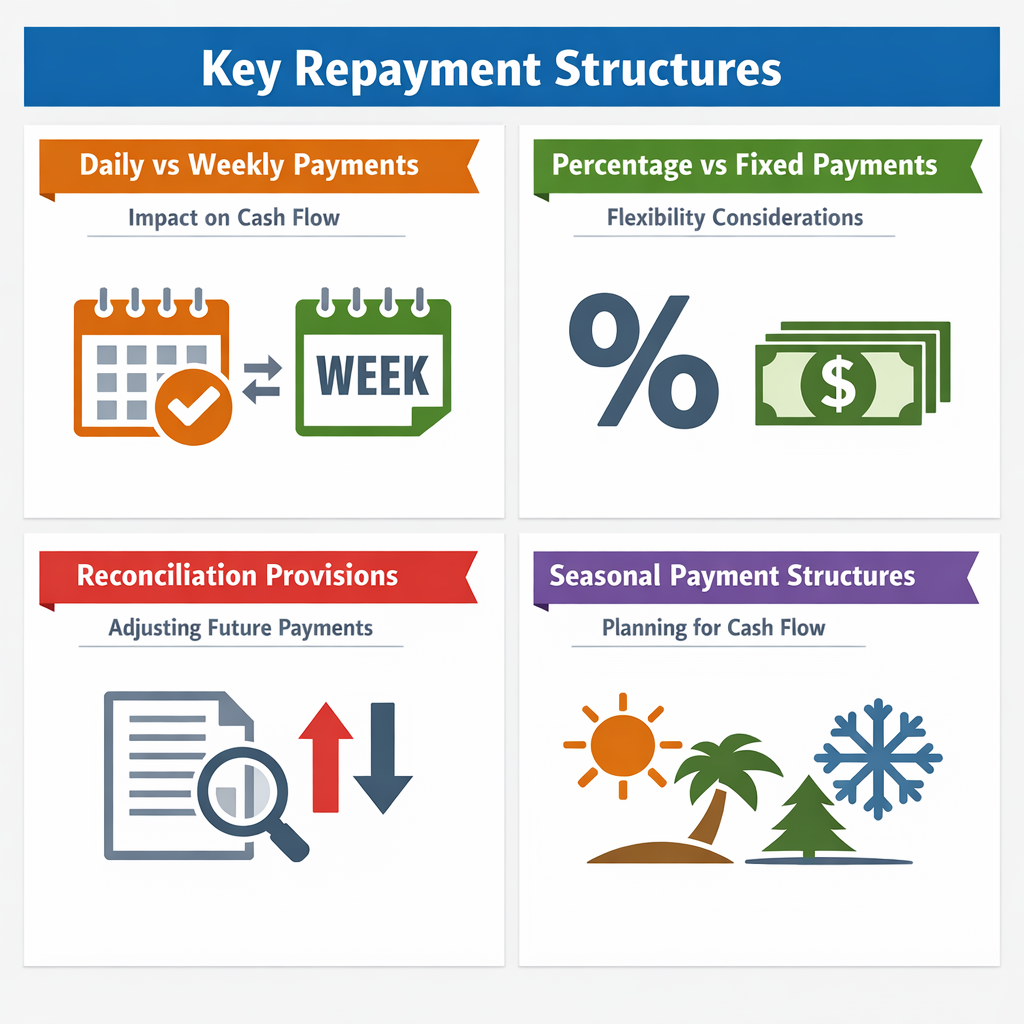

Repayment Rules That Affect Your Cash Flow

Repayment rules that affect your cash flow are among the most critical aspects of any funding agreement, yet they're frequently misunderstood by business owners focused on immediate capital needs.

- Daily versus weekly remittance structures: The frequency of payments can significantly impact your working capital. Daily deductions from revenue might seem small individually but can create cumulative pressure on cash reserves, especially during slower sales periods.

- Percentage-based versus fixed payment models: Understanding whether your repayment is tied to a percentage of sales or a fixed amount is crucial. Percentage-based arrangements typically adjust with your revenue, which can provide flexibility during slower months but may also extend your repayment period.

- Reconciliation and true-up provisions: Some agreements include periodic reconciliation clauses that adjust future payments based on actual revenue versus projected figures. These adjustments could result in sudden payment increases that strain your budget.

- Holiday and seasonal payment structures: Not all agreements account for seasonal variations in your business. Understanding how payments are calculated during traditionally slower periods can help you plan for potential cash flow challenges.

Each of these repayment structures carries different implications for your day-to-day operations. What works well for one business might create difficulties for another, depending on revenue patterns, profit margins, and operational expenses. By thoroughly understanding these rules before committing, you can better assess whether a particular funding arrangement aligns with your business's financial rhythm.

Fine Print Provisions You Should Never Ignore

Fine print provisions you should never ignore often contain risk-shifting clauses that quietly transfer responsibilities and liabilities in ways that could affect your financial operations.

- Confession of judgment clauses: These provisions allow the funding provider to obtain a judgment against you without a traditional court process. If included, they significantly reduce your ability to dispute issues or negotiate if problems arise.

- Venue and jurisdiction specifications: Where disputes must be resolved can impact both the cost and complexity of any legal proceedings. Agreements that require resolution in distant locations can make it prohibitively expensive to defend your interests.

- Waiver of jury trial rights: Some contracts ask you to waive your right to a jury trial in disputes. This changes the nature of how conflicts would be resolved and might affect the outcome of any disagreements.

- Indemnification requirements: These clauses might require you to compensate the funding provider for certain losses or legal costs, even in situations where the issue wasn't directly your fault. The scope of these obligations can be broader than initially apparent.

While these provisions might seem like standard legal language, they can have substantive implications on your rights and protections. Many business owners overlook these sections because they appear technical or assume they're non-negotiable. However, recognizing these elements allows you to ask questions, seek clarification, and potentially negotiate better agreements that better protect your interests.

Understanding Prepayment and Early Termination Terms

Understanding prepayment and early termination terms is essential because they determine your flexibility if your business circumstances change or you find better funding options.

- Prepayment penalties and their calculation: Many agreements charge fees if you pay off your funding early. These penalties can be calculated in various ways, from flat fees to percentages of the remaining balance, and might negate much of the benefit you'd gain from early repayment.

- Minimum term requirements: Some contracts lock you into a minimum period regardless of how quickly you repay the principal amount. This means you could be obligated to pay the full expected cost even if you generate the funds to repay early.

- Partial prepayment restrictions: Even if full prepayment is allowed, some agreements restrict partial prepayments or require minimums for any early payment. This limits your ability to gradually reduce your obligations as cash flow improves.

- Refinancing implications: Certain contracts include provisions that affect your ability to refinance with another provider, either through explicit restrictions or financial penalties that make refinancing economically unfeasible.

These terms directly affect your financial flexibility and should be carefully evaluated against your business plans. If you anticipate strong growth or seasonal revenue spikes that might allow early repayment, understanding these provisions helps you calculate the true cost of your funding over time. In some cases, the restrictions might make one funding option less attractive than another, even if the initial terms seem comparable.

Steps to Thoroughly Review Your Funding Agreement

Steps to thoroughly review your funding agreement can help you avoid unexpected complications and ensure you fully understand your obligations before signing.

- Request the complete agreement in advance: Don't wait until the closing meeting to see your full contract. Ask for all documents at least 48 hours before you're expected to sign, giving yourself adequate time to review everything carefully without pressure.

- Create a terms comparison sheet: If you're evaluating multiple funding options, build a simple spreadsheet comparing key terms side by side. Include total cost, repayment structure, fees, penalties, and any special provisions. This visual comparison often reveals differences that aren't obvious when reading contracts separately.

- Identify and highlight unclear provisions: As you read through the agreement, mark any section you don't fully understand or that uses ambiguous language. Prepare specific questions about these sections rather than glossing over them or assuming they're not important.

- Calculate the total cost under different scenarios: Work through the math for best-case, typical, and challenging business scenarios. Understanding how much you'll actually pay under various circumstances helps you assess whether the funding remains affordable even if revenue doesn't meet optimistic projections.

- Verify all verbal promises appear in writing: Any assurance or promise made during discussions should be reflected in the written agreement. If something was discussed but doesn't appear in the contract, it typically isn't enforceable, so clarify these discrepancies before signing.

Taking these steps might seem time-consuming, but the investment of a few extra hours can prevent months or years of financial complications. Many disputes and financial difficulties arise not from dishonest practices but from genuine misunderstandings about what was agreed upon. A methodical review process helps ensure both you and your funding provider have the same understanding of your arrangement.

Questions to Ask Before Finalizing Any Funding Deal

Questions to ask before finalizing any funding deal can clarify ambiguities and reveal information that might not be volunteered but could significantly impact your experience.

- What happens if my business experiences a temporary slowdown? Understanding how the provider handles situations where you need temporary relief can reveal a lot about the flexibility of the arrangement and the working relationship you can expect.

- Are there any circumstances where fees could increase? Beyond the stated rates and fees, ask whether any conditions could trigger additional costs. Some agreements include provisions for administrative fees, late fees, or other charges that only apply under certain circumstances.

- How is my payment calculated if I have revenue fluctuations? If your repayment is tied to revenue, clarify exactly how that calculation works, what revenue sources are included, and how often adjustments are made. Understanding this prevents surprises when payments don't match your expectations.

- What reporting or documentation will I need to provide? Some arrangements require ongoing financial reporting, bank statements, or other documentation. Knowing these requirements helps you assess the administrative burden and ensures you can comply without difficulty.

- Can you explain this specific clause in plain language? Don't hesitate to ask about any provision that seems complex or confusing. A reputable provider should be willing and able to explain every element of your agreement in terms you can understand without legal training.

Asking thorough questions demonstrates that you're a careful business owner who takes financial obligations seriously. Most funding providers appreciate working with informed clients because it tends to result in smoother relationships and fewer misunderstandings. If a provider seems reluctant to answer questions or dismisses your concerns as unimportant, that response itself might be valuable information about whether this is the right funding partner for your business.

Understanding funding terms most businesses overlook isn't about being suspicious or distrustful. It's about being informed and prepared to make decisions that truly serve your business's best interests. The research consistently shows that inadequate preparation and oversight of contract details can lead to unfavorable outcomes that might have been avoided with more careful attention.

By familiarizing yourself with common hidden clauses, repayment structures, fine print provisions, and termination terms, you position yourself to negotiate more effectively and select funding arrangements that align with your operational reality. The questions you ask and the time you invest in review before signing can prevent complications that might otherwise affect your cash flow and financial stability.

Remember that every clause in a funding agreement represents a specific allocation of risk and responsibility. Treating these documents as substantive rather than mere formalities helps ensure you're entering partnerships with clear expectations on both sides. Whether you're seeking your first funding arrangement or refinancing existing obligations, the principles outlined here can guide you toward better outcomes.