.png)

When it comes to understanding merchant cash advance terms, many small business owners find themselves overwhelmed by complex agreements and unfamiliar terminology. Unlike traditional financing options, merchant cash advances operate with unique structures that can significantly impact your business's cash flow and financial health. With technological advancements and shifting regulatory standards influencing the industry in 2025, it's more important than ever to grasp these fundamental concepts before entering into any agreement.

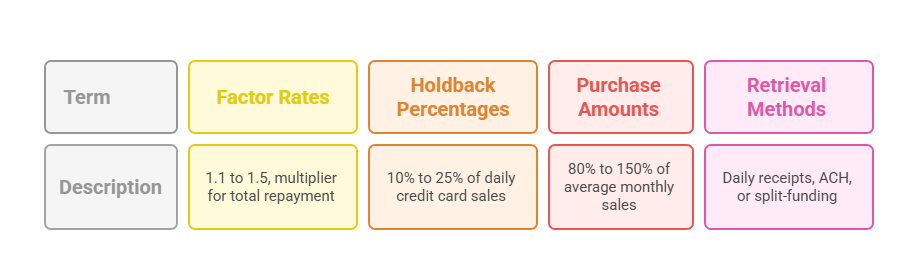

Essential Components of MCA Agreements

The foundation of understanding merchant cash advance terms lies in recognizing the key elements that make up these financing agreements. Each component plays a crucial role in determining the total cost and impact on your business operations.

- Factor rates typically range from 1.1 to 1.5, representing the multiplier applied to your advance amount to determine total repayment

- Holdback percentages usually fall between 10% and 25% of your daily credit card sales, directly affecting your available cash flow

- Purchase amounts can vary widely based on your monthly revenue, with providers often offering advances equal to 80% to 150% of your average monthly sales

- Retrieval methods may include daily credit card receipts, ACH withdrawals, or split-funding arrangements that impact how quickly you repay the advance

How Factor Rates Impact Total Cost

Factor rates represent one of the most critical aspects when understanding merchant cash advance terms, as they directly determine your total repayment amount. Unlike traditional interest rates, factor rates are fixed multipliers that don't change based on how quickly you repay the advance.

- Calculation simplicity makes factor rates easy to understand, as you multiply your advance amount by the factor rate to get your total repayment

- Cost comparison challenges arise because factor rates don't translate directly to annual percentage rates, making it harder to compare with other financing options

- No early payoff benefits exist with factor rates, meaning you'll pay the same total amount whether you repay in three months or twelve months

- Industry variations may occur based on your business type, with some industries receiving more favorable factor rates due to perceived lower risk

Holdback Percentage and Cash Flow Management

The holdback percentage represents the portion of your daily sales that goes toward repaying your merchant cash advance, making it a crucial factor in understanding merchant cash advance terms and their impact on your business operations.

- Daily cash flow reduction occurs when providers collect their percentage, potentially affecting your ability to cover operating expenses during slower sales periods

- Seasonal business considerations become important if your revenue fluctuates throughout the year, as holdback amounts will vary with your sales volume

- Multiple advance complications can arise if you have more than one MCA, as combined holdback percentages might consume too much of your daily revenue

- Negotiation opportunities may exist for established businesses with strong sales histories, potentially securing lower holdback percentages

Repayment Timeline Variables and Expectations

Understanding merchant cash advance terms includes recognizing that repayment structures aren't fixed like traditional financing, instead fluctuating based on your business's daily sales performance and the agreed-upon holdback percentage.

- Sales-dependent duration means your repayment period will extend during slower months and shorten during peak sales periods

- Average timeframe estimates typically range from 3 to 18 months, though actual timelines depend entirely on your business's sales velocity

- Weekend and holiday impacts can extend repayment periods if your business doesn't process sales during these times

- Reconciliation processes may occur periodically to ensure collections align with actual sales data, potentially adjusting future holdback amounts

Smart Evaluation Steps for MCA Terms

Making informed financing decisions requires a systematic approach to understanding merchant cash advance terms and their long-term implications for your business. These steps can help you navigate the evaluation process effectively.

- Calculate true costs by converting factor rates to annualized percentages based on estimated repayment timelines to compare with other financing options

- Model cash flow impacts using different scenarios to understand how holdback percentages will affect your daily operations during various sales periods

- Review regulatory protections available in your state, as new safeguards implemented since 2023 may provide additional security and transparency

- Consider timing alternatives by evaluating whether waiting for traditional financing might be more cost-effective than accepting higher MCA costs

- Negotiate specific terms such as holdback percentages or factor rates, especially if you have strong sales history or are considering multiple offers

Understanding merchant cash advance terms requires careful attention to factor rates, holdback percentages, and repayment structures that can significantly impact your business's financial health. While these advances offer quick access to capital, the unique terminology and cost structures demand thorough evaluation before committing to any agreement. With evolving industry standards and regulatory protections now available in many states, business owners have more tools than ever to make informed decisions. Take time to model different scenarios, compare total costs with alternative financing options, and leverage regulatory safeguards to secure the most favorable terms for your specific situation.