.png)

Many business owners find themselves surprised by the actual cost of their merchant cash advance after signing on the dotted line. Understanding the true cost of your advance requires looking beyond the advertised factor rate to uncover what you'll really pay over time.

Factor Rate vs APR: Key Differences

The distinction between factor rate vs APR often confuses business owners seeking quick funding. Factor rates appear straightforward but can mask the actual annual cost of your advance.

- Factor rates remain constant throughout repayment, typically ranging from 1.1 to 1.5, meaning you might pay $1,100 to $1,500 for every $1,000 advanced

- APR represents the annualized cost including fees, making it easier to compare with traditional financing options

- Factor rates don't account for repayment speed, while APR calculations consider the time element of borrowing costs

- Converting factor rates to APR often reveals significantly higher costs than initially apparent

Hidden Fees That Impact Your Total Cost

Beyond the advertised rate, various fees can substantially increase your financing costs. These charges may not be immediately obvious during initial discussions.

- Origination fees that get deducted from your advance amount upfront

- Processing fees for daily or weekly payment collections from your bank account

- Early payoff penalties that discourage settling your balance ahead of schedule

- Administrative charges for account maintenance and customer service

- Late payment fees if your daily sales fall below expected collection amounts

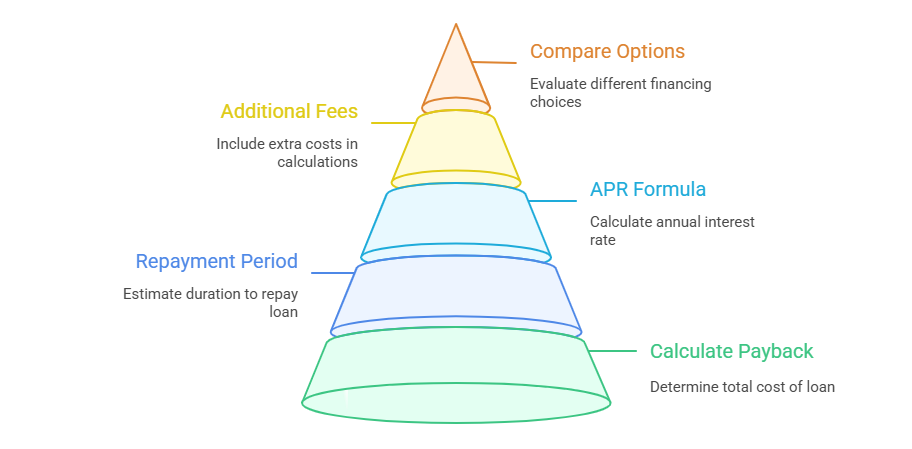

Effective Rate Analysis Steps

Conducting an effective rate analysis helps you understand exactly what your advance will cost annually. This process requires converting the factor rate into comparable terms.

- Calculate your total payback amount by multiplying your advance by the factor rate

- Determine your repayment period based on projected daily sales and collection percentage

- Apply the APR formula using total cost, principal amount, and time period to find your annualized rate

- Add any additional fees to get your complete cost picture

- Compare this final number with other financing options available to your business

Cost Transparency in Advance Agreements

Cost transparency should be a primary consideration when evaluating advance providers. Some companies provide clearer disclosure than others regarding total costs.

Review all documentation carefully before signing, paying special attention to fee schedules and payment terms. Ask providers to explain how faster or slower sales might affect your total costs.

Request examples showing different repayment scenarios and their associated costs. This information helps you prepare for various business conditions that could impact your advance repayment timeline.

Document all verbal promises about rates and fees in writing. Clear agreements protect both parties and prevent misunderstandings about advance costs down the road.

Understanding the true cost of your advance protects your business from unexpected expenses and helps you make informed financing decisions. Take time to convert factor rates to APR, identify all potential fees, and compare total costs across different providers before committing to any advance agreement.