.png)

Managing cash flow in retail isn't just about tracking what comes in and goes out. It's about understanding the rhythm of your business and making smart decisions that keep money flowing when you need it most. Working capital insights for retail owners can make the difference between thriving during peak seasons and struggling to keep the lights on during slower periods.

Retail businesses face unique challenges that other industries don't typically encounter. Your inventory needs to be stocked before customers walk through the door, suppliers often require deposits or quick payments, and seasonal sales can create dramatic swings in cash availability. These factors make working capital management both critical and complex for retail operations.

Understanding Your Retail Cash Flow Patterns

Understanding your retail cash flow patterns forms the foundation of effective working capital management. Every retail business has its own unique rhythm that reflects customer behavior, seasonal trends, and operational requirements.

- Track seasonal fluctuations: Most retail businesses experience predictable peaks and valleys throughout the year. Holiday seasons might bring increased sales, while certain months could see dramatic drops in customer traffic.

- Monitor inventory turnover cycles: Different products move at different speeds, and understanding these patterns helps you allocate cash more effectively. Fast-moving items require frequent restocking, while slower inventory ties up capital for longer periods.

- Analyze payment timing gaps: The time between when you pay suppliers and when customers pay you creates cash flow gaps that need careful management. These gaps often widen during growth periods or seasonal buildups.

- Identify recurring operational expenses: Rent, utilities, payroll, and insurance create predictable cash outflows that must be balanced against variable sales income.

Strategic Inventory Management for Better Liquidity

Strategic inventory management for better liquidity requires balancing customer demand with cash availability. Your inventory represents a significant portion of your working capital, and managing it effectively can free up substantial funds for other business needs.

- Implement just-in-time ordering: Order inventory closer to when you'll actually sell it, reducing the amount of cash tied up in unsold merchandise. This approach requires good supplier relationships and accurate demand forecasting.

- Negotiate flexible payment terms: Work with suppliers to establish payment schedules that align with your cash flow cycles. Extended payment terms or seasonal adjustments can provide breathing room during tight periods.

- Focus on high-turnover products: Prioritize inventory investments in items that sell quickly and reliably. These products generate faster returns on your cash investment and reduce storage costs.

- Monitor slow-moving inventory: Regularly review items that aren't selling and develop strategies to move them, such as bundling, discounting, or returning to suppliers when possible.

Managing Seasonal Sales and Cash Requirements

Managing seasonal sales and cash requirements involves preparing for predictable fluctuations while maintaining financial stability year-round. Seasonal sales challenges face unique working capital challenges that require proactive planning and flexible financing strategies.

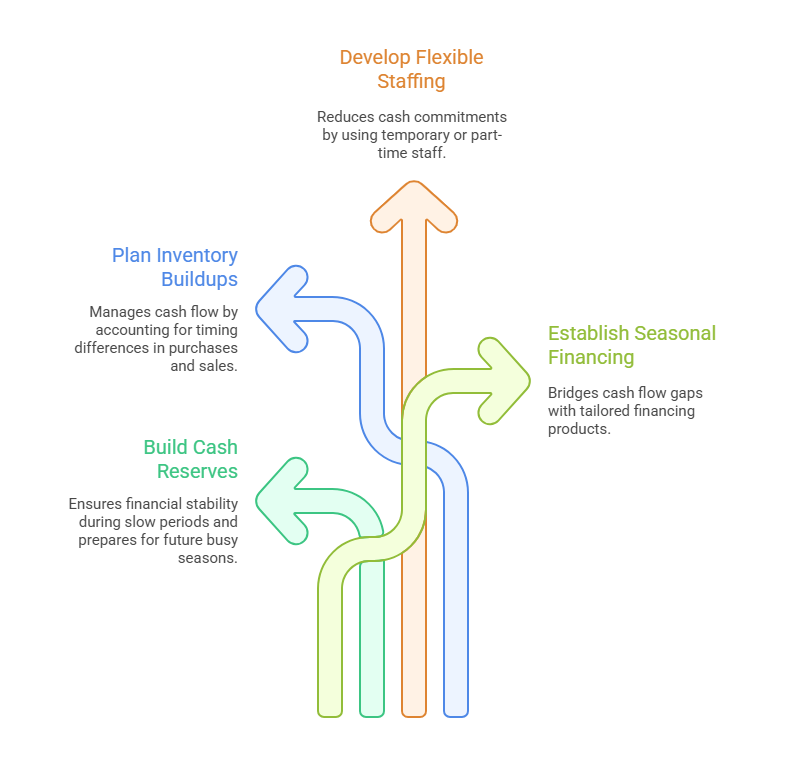

- Build cash reserves during peak periods: When seasonal sales are strong, resist the urge to spend all the extra cash immediately. Set aside funds to carry you through slower periods and prepare for the next busy season.

- Plan inventory buildups carefully: Seasonal inventory purchases often require significant cash outlays months before sales occur. Create detailed cash flow projections that account for these timing differences.

- Develop flexible staffing strategies: Seasonal sales typically require additional staff, but permanent hires create ongoing cash commitments. Consider temporary workers, part-time positions, or performance-based compensation during peak periods.

- Establish seasonal financing arrangements: Many lenders understand seasonal retail patterns and offer financing products designed to bridge cash flow gaps during slower periods or inventory buildups.

Optimizing Supplier Relationships and Payment Terms

Optimizing supplier relationships and payment terms can significantly improve your working capital position without requiring additional external financing. Strong supplier partnerships create opportunities for more favorable cash flow arrangements.

- Negotiate extended payment terms: Many suppliers will extend payment periods for reliable customers, giving you more time to sell merchandise before payment is due. Even an extra 15-30 days can make a substantial difference in cash flow.

- Explore consignment arrangements: Some suppliers might agree to consignment deals where you pay only after items sell. This arrangement virtually eliminates inventory carrying costs and reduces liquidity risk.

- Request volume discounts: Larger orders often qualify for better pricing, but balance these savings against the cash flow impact of bigger inventory investments and longer holding periods.

- Establish credit lines with key suppliers: Trade credit from suppliers often costs less than bank financing and aligns payment obligations with your sales cycles more naturally than traditional financing.

Action Steps for Improved Working Capital Management

Action steps for improved working capital management transform insights into practical results. Implementation requires systematic approaches that address the most impactful areas first while building sustainable management practices.

- Conduct a comprehensive cash flow analysis: Review 12-24 months of financial data to identify patterns, gaps, and opportunities. This analysis should include seasonal trends, inventory cycles, and supplier payment obligations to create a complete picture of your working capital needs.

- Develop monthly cash flow projections: Create rolling 6-month forecasts that account for seasonal variations, planned inventory purchases, and expected sales patterns. Update these projections monthly based on actual results and changing market conditions.

- Establish working capital targets and metrics: Set specific goals for inventory turnover, cash conversion cycles, and liquidity ratios. Track these metrics regularly to identify trends and make adjustments before problems become serious.

- Create contingency plans for cash shortfalls: Identify potential sources of additional working capital, such as financing options, asset-based lending, or supplier credit extensions. Having these arrangements in place before you need them provides security and often better terms.

- Review and optimize all working capital components quarterly: Regularly assess inventory levels, accounts receivable practices, supplier terms, and cash management procedures. Small improvements in multiple areas can create significant overall improvements in working capital efficiency and help optimize cash flow for retail owners.

Effective working capital management separates successful retail operations from those that struggle with cash flow challenges. The strategies outlined here might seem straightforward, but their consistent application can transform how your business handles financial ups and downs.

Remember that working capital insights for retail owners aren't just about surviving slow periods or managing inventory cycles. They're about creating the financial foundation that allows your business to grow, take advantage of opportunities, and weather unexpected challenges with confidence.

Start by focusing on the areas where you can make the biggest impact quickly, such as negotiating better supplier terms or improving inventory turnover. As these improvements take hold, you'll find that managing seasonal sales fluctuations and reducing liquidity risk becomes much more manageable.