.png)

Economic downturns create significant challenges for small business owners seeking funding. With the U.S. economy experiencing contractions and investment declining, understanding how to navigate recession financing becomes crucial for business survival.

Common Questions About Recession Financing

Q: How does an economic downturn affect my ability to get business funding?

During economic contractions, lenders typically tighten their underwriting standards and may reduce approval rates. Financial institutions become more conservative with their lending practices, requiring stronger financial documentation and potentially offering less favorable terms. This shift means businesses need to prepare for more rigorous risk assessments and potentially higher borrowing costs.

Q: Should I wait for economic conditions to improve before seeking funding?

Waiting might not be the best strategy. Economic recovery timelines remain uncertain, and businesses often need capital to maintain operations during challenging periods. Proactively exploring diverse financing options while you still have strong cash flow positions you better than waiting until financial strain becomes severe.

Q: Are interest rates always higher during economic downturns?

Not necessarily. Recent trends show that some interest rates have actually declined, which could benefit qualifying businesses. However, approval standards may become stricter, meaning fewer businesses might qualify despite potentially lower rates.

Understanding Current Economic Challenges

The current economic landscape presents unique challenges for small businesses seeking funding. Investment in structures has declined significantly, with some forecasts showing continued economic headwinds ahead. These conditions create a ripple effect that impacts lending availability and terms.

Small businesses face elevated costs across multiple areas including goods, wages, and financing itself. This triple pressure makes cash flow management more critical than ever. The economic contraction has led many financial institutions to manage their exposure limits more carefully, resulting in more competitive and selective funding processes.

Despite these challenges, some positive trends have emerged. Certain interest rates have shown decline, potentially reducing borrowing costs for businesses that can meet stricter qualification requirements. However, approval rates at some financial institutions have decreased, indicating that lender tightening continues to affect access to traditional financing options.

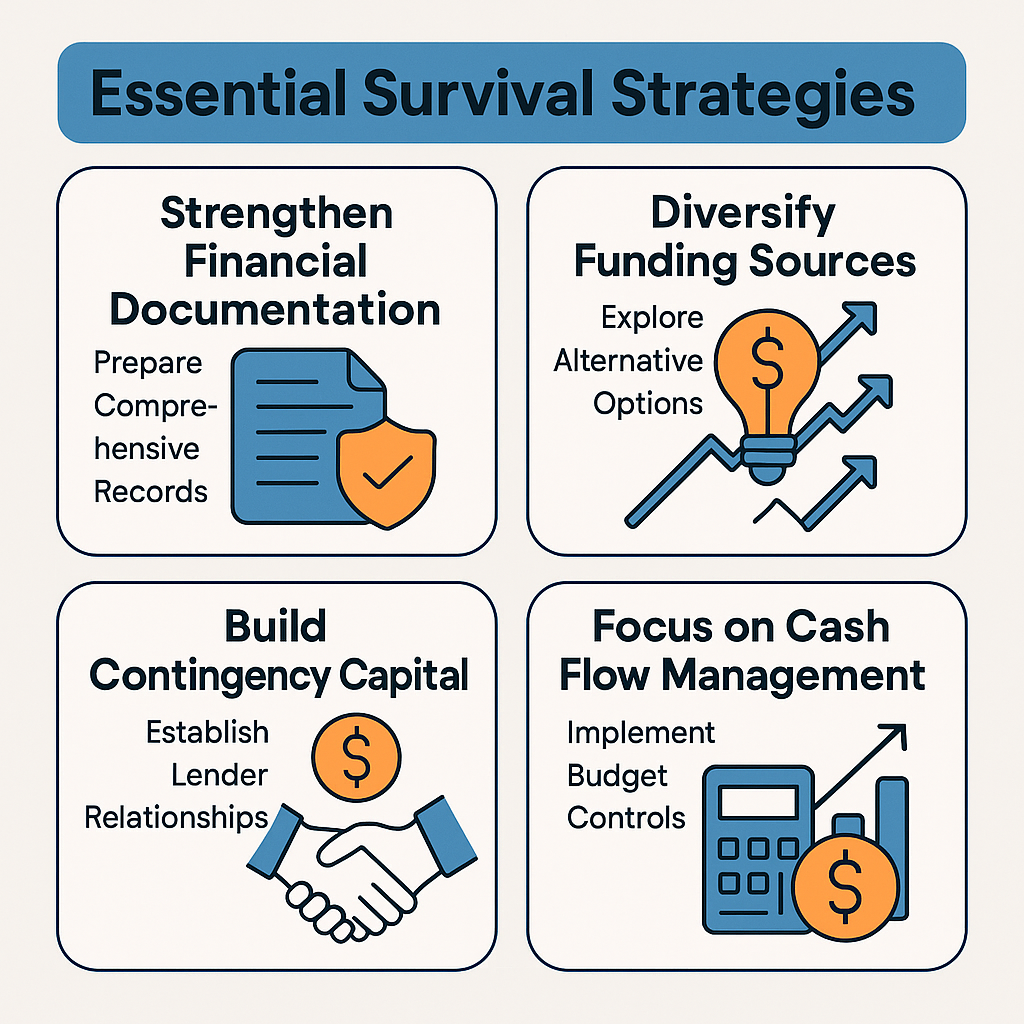

Essential Survival Strategies During Downturns

- Strengthen Financial Documentation: Prepare comprehensive financial records, cash flow projections, and business plans. Lenders conduct more thorough reviews during economic uncertainty, so having detailed documentation readily available can speed up the approval process.

- Diversify Funding Sources: Avoid relying on a single financing option. Explore alternative lenders, merchant cash advances, and other non-traditional funding sources that may have different approval criteria than conventional banks.

- Build Contingency Capital: Establish relationships with multiple lenders before you need funding. Having pre-approved credit lines or established relationships can provide faster access to capital when opportunities or emergencies arise.

- Focus on Cash Flow Management: Implement stricter budget controls and identify areas where costs can be reduced without affecting core operations. Strong cash flow demonstrates financial stability to potential lenders.

Risk Pricing and Lender Evaluation Factors

- Industry Resilience: Lenders may favor businesses in sectors that historically perform better during economic downturns. Understanding how your industry is perceived can help you position your funding application more effectively.

- Revenue Stability: Demonstrate consistent revenue streams or explain how your business model adapts to economic changes. Lenders look for businesses that can maintain operations even when consumer spending decreases.

- Debt-to-Income Ratios: Economic uncertainty makes lenders more sensitive to existing debt obligations. Reducing unnecessary debt before applying for new funding can improve your risk profile.

- Collateral and Personal Guarantees: Be prepared for requests for additional security. Lenders may require more collateral or personal guarantees to offset perceived increased risk during economic downturns.

Business funding during economic downturns requires strategic planning and adaptability. While lenders may implement stricter standards, opportunities still exist for well-prepared businesses. Focus on strengthening your financial position, diversifying funding sources, and building relationships with multiple lenders to improve your chances of securing the capital you need to weather economic challenges.