.png)

Understanding how lenders assess business performance can make the difference between funding approval and rejection. When you're seeking financing for your business, lenders don't just look at a single number or metric. Instead, they use comprehensive evaluation methods to determine your company's creditworthiness and repayment capacity.

The lending landscape has evolved significantly, with modern financial institutions employing sophisticated tools and models to analyze business performance. From gross revenue analysis to seasonal variation patterns, lenders examine multiple facets of your operation to build a complete risk profile.

Financial Documentation Requirements

Financial documentation requirements form the foundation of how lenders assess business performance. These documents provide the raw data that feeds into sophisticated credit scoring models and risk assessment frameworks.

- Bank statements and cash flow records that demonstrate your business's ability to generate consistent revenue streams

- Tax returns and financial statements that offer a comprehensive view of your company's financial health over multiple years

- Profit and loss statements that reveal operational efficiency and expense management capabilities

- Balance sheets that show your business's assets, liabilities, and overall financial position

Revenue Analysis Methods

Revenue analysis methods represent a critical component in how lenders assess business performance, focusing on both current earnings and future potential. Gross revenue analysis helps lenders understand the scale and trajectory of your business operations.

- Monthly recurring revenue tracking to identify stability and growth patterns in your income streams

- Revenue diversification assessment to evaluate risk concentration and customer dependency levels

- Year-over-year growth calculations that demonstrate your business's expansion potential and market position

- Revenue per customer analysis to understand the value and sustainability of your customer relationships

Consistency Metrics Evaluation

Consistency metrics evaluation plays a vital role in how lenders assess business performance, as predictable cash flow often matters more than high but volatile earnings. These metrics help lenders gauge your repayment capacity over time.

- Cash flow consistency scores that measure the predictability of your monthly and quarterly earnings

- Payment history analysis to evaluate your track record with existing financial obligations and vendor relationships

- Operational stability indicators such as employee retention rates and customer churn statistics

- Expense management patterns that demonstrate your ability to maintain cost control during different business cycles

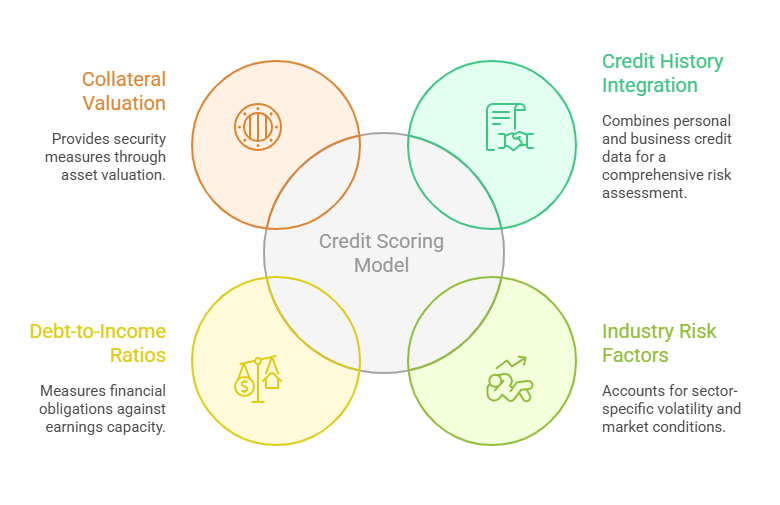

Credit Scoring Model Components

Credit scoring model components form the technical backbone of how lenders assess business performance in today's data-driven lending environment. These models create comprehensive risk profiles by analyzing multiple data points simultaneously.

- Personal and business credit history integration that combines your individual creditworthiness with your company's financial track record

- Industry-specific risk factors that account for sector volatility and market conditions affecting your business type

- Debt-to-income ratios and leverage calculations that measure your current financial obligations relative to earnings capacity

- Collateral and asset valuations that provide security measures for the lending institution's risk management

Seasonal Variation Impact

Seasonal variation impact significantly influences how lenders assess business performance, particularly for companies with cyclical revenue patterns. Understanding these patterns helps lenders predict cash flow during different periods throughout the year.

- Historical seasonal trend analysis to identify recurring patterns in your business's peak and slow periods

- Cash reserve management during off-seasons that demonstrates your ability to maintain operations year-round

- Revenue smoothing strategies such as diversified product lines or service offerings that reduce seasonal dependency

- Inventory and working capital adjustments that show your business can adapt to changing seasonal demands effectively

Key Preparation Strategies

Preparing for the lending process becomes much more effective when you understand exactly how lenders assess business performance. By aligning your documentation and presentation with lender expectations, you can significantly improve your chances of securing favorable financing terms. Focus on presenting a clear narrative that demonstrates financial stability, growth potential, and strong repayment capacity. Organize your financial records chronologically and ensure all documentation is current and accurate. Consider working with financial professionals who understand lending requirements and can help you present your business in the best possible light to potential lenders.

Understanding how lenders assess business performance gives you a significant advantage in the funding process. By focusing on the key areas that matter most to lenders, from gross revenue analysis to consistency metrics, you can position your business for success. Remember that lenders want to see predictable cash flow, strong financial management, and clear repayment capacity.

Take time to review your financial documentation, address any weaknesses in your business performance metrics, and present a compelling case for your funding needs. The investment you make in understanding and preparing for the lender evaluation process often pays dividends in better terms, higher approval rates, and stronger relationships with financial institutions.