.png)

Securing business funding can feel like navigating a maze, especially when you're not sure what affects your business funding eligibility. Understanding these factors isn't just helpful, it's crucial for your success. Lenders evaluate multiple elements before approving financing, from your monthly revenue patterns to your industry's risk profile.

The funding landscape has evolved significantly, with different types of lenders offering varying approval criteria. While larger financial institutions might have stricter requirements, smaller banks and credit unions often provide more favorable odds for small business owners. This shift means knowing where to apply can be just as important as having the right financial profile.

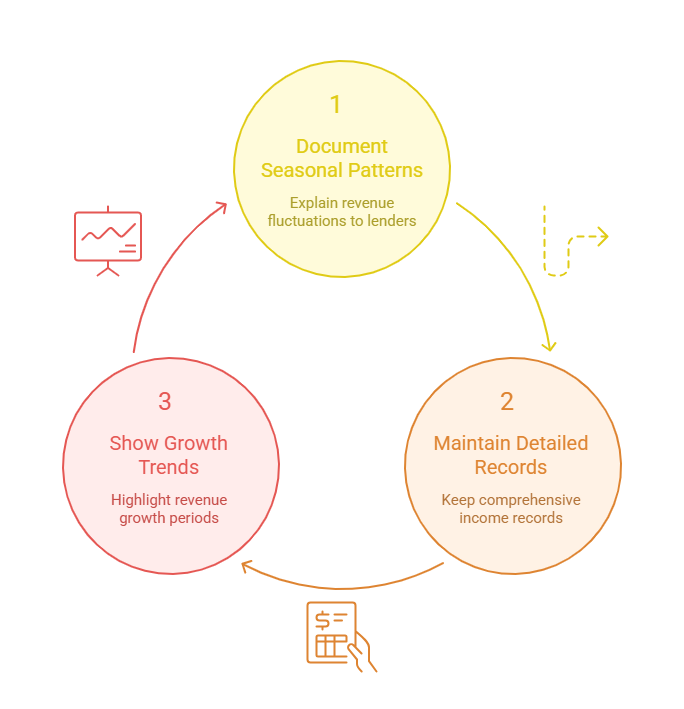

Essential Tips for Strengthening Your Monthly Revenue Profile

Your monthly revenue profile serves as the foundation of what affects your business funding eligibility. Lenders typically want to see consistent income streams that demonstrate your ability to handle regular payments.

- Document seasonal patterns clearly: If your business experiences seasonal fluctuations, prepare explanations and show how you manage cash flow during slower periods. This transparency helps lenders understand your revenue cycles rather than viewing dips as red flags.

- Maintain detailed revenue records: Keep comprehensive records of all income sources, including digital payments, cash transactions, and recurring contracts. Clean documentation makes the underwriting process smoother and builds credibility with potential lenders.

- Show growth trends when possible: Even modest upward trends in revenue can significantly impact your eligibility. Highlight periods of growth and explain the strategies that drove those improvements to demonstrate business momentum.

Key Strategies for Improving Bank Statement Health

Bank statement health represents one of the most scrutinized aspects of what affects your business funding eligibility. Your statements tell the story of your financial management and cash flow stability.

- Minimize overdrafts and negative balances: Frequent overdrafts signal poor cash flow management to lenders. Focus on maintaining positive balances and consider setting up alerts to prevent accidental overdrafts that could harm your application.

- Separate business and personal transactions: Mixed transactions create confusion and may raise questions about your financial organization. Use dedicated business accounts and avoid personal withdrawals that could complicate the review process.

- Maintain consistent deposit patterns: Regular deposits show steady business activity, while erratic patterns might suggest instability. If you have irregular income, consider explaining your business model upfront to provide context for unusual deposit schedules.

Managing Industry Risk Factors Effectively

Industry risk plays a significant role in what affects your business funding eligibility, though it's often beyond your direct control. Different sectors carry varying levels of perceived risk in lenders' eyes.

- Research lender preferences for your industry: Some lenders specialize in high-risk industries while others avoid them entirely. Targeting the right lenders can save time and improve your approval chances significantly.

- Prepare industry-specific documentation: High-risk industries may need additional documentation such as licenses, insurance policies, or compliance certificates. Having these ready demonstrates professionalism and preparedness to potential lenders.

- Emphasize stability factors unique to your business: Even in risky industries, you can highlight elements that reduce your specific risk profile, such as long-term contracts, diversified customer bases, or proven track records during economic downturns.

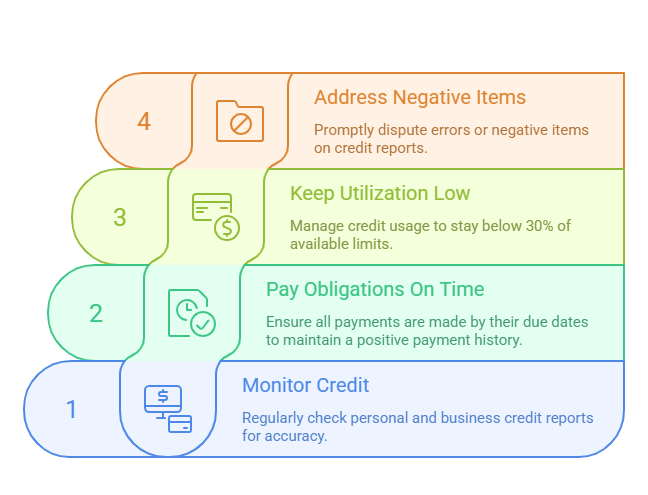

Steps to Build and Maintain Credit Stability

Credit stability forms a cornerstone of what affects your business funding eligibility, encompassing both business and personal credit profiles. Here's how to strengthen this crucial factor:

- Monitor both personal and business credit regularly: Many business owners focus only on business credit, but lenders often review personal credit too, especially for smaller businesses. Regular monitoring helps you catch and address issues before they impact funding applications.

- Pay all obligations on time consistently: Payment history carries significant weight in credit scoring. Set up automated payments for recurring obligations and maintain a calendar for other due dates to avoid missed payments that could damage your profile.

- Keep credit utilization ratios low: High utilization on business credit lines or cards can signal financial stress. Aim to keep utilization below 30% of available limits, and consider requesting limit increases to improve your ratios if needed.

- Address negative items promptly: If you discover errors or negative items on your credit reports, dispute them quickly through proper channels. Sometimes legitimate issues can be resolved through direct communication with creditors before they escalate.

Choosing the Right Lenders for Your Business Profile

Understanding what affects your business funding eligibility includes knowing which lenders align with your specific situation. The lending landscape offers various options with different criteria and approval rates.

- Target smaller banks and credit unions first: Research indicates that smaller financial institutions often have higher approval rates compared to major banks. These lenders may be more willing to work with local businesses and consider factors beyond strict algorithmic criteria.

- Compare terms and conditions thoroughly: Interest rates represent just one component of financing costs. Evaluate fees, repayment terms, and any additional requirements that could impact your business operations or cash flow management strategies.

- Consider alternative lending options: Traditional banks aren't your only choice. Alternative lenders may have different eligibility criteria that better match your business profile, though terms and rates can vary significantly across this category.

- Research lender specializations: Some lenders focus on specific industries, business sizes, or geographic regions. Finding lenders that specialize in your sector might improve your approval chances and lead to better terms.

Additional Factors That Impact Funding Decisions

Beyond the primary elements, several other factors contribute to what affects your business funding eligibility. Understanding these can help you present a stronger application.

- Business age and operational history: Newer businesses often face additional scrutiny, while established businesses with longer track records may enjoy more favorable treatment from lenders who can review historical performance patterns.

- Collateral and personal guarantees: The availability of assets to secure financing can significantly impact both approval odds and terms. Consider what assets might be available and understand the implications of personal guarantees before committing.

- Cash flow projections and business plans: Well-prepared financial projections and comprehensive business plans demonstrate professionalism and forward-thinking that lenders appreciate, especially when seeking larger funding amounts.

- Existing debt obligations: Current debt levels affect your debt-to-income ratios and available cash flow for new payments. Lenders evaluate whether additional debt payments fit comfortably within your financial capacity.

Understanding what affects your business funding eligibility empowers you to take control of your financing journey. From maintaining strong monthly revenue patterns and healthy bank statements to managing industry risk factors and building credit stability, each element plays a vital role in your success.

Remember that different lenders may weight these factors differently, making it important to research and target the right financial institutions for your specific situation. Smaller banks and credit unions often provide better approval rates, while alternative lenders might offer solutions for businesses that don't fit traditional criteria.

The key lies in preparation and presentation. By strengthening these core areas and understanding how lenders evaluate applications, you're positioning your business for funding success. Take time to assess your current standing in each area, address any weaknesses, and approach the right lenders with confidence in your financial profile.